Before I write this article, let me thank our senior portfolio analyst Eric Rossman, who simply smiled when I handed him a doozey of a research question.

Specifically, I asked, what is compound annual change and absolute change of the dividend payout ratio for the S&P 500 and each of its constituent companies?

This was no small order. Thank you Eric!

I wanted to know this to properly advise our clients, especially those looking for income in a low yield environment.

You see, there are plenty of companies that pay high dividends. But the risk is this: if the company cuts the dividend, not only is there a loss of income, but the loss of confidence that often comes with a cut in the dividend can result in loss of principal. And a la Warren Buffet: Rule One: Never Lose Money. Rule Two: Never Forget Rule One.

The dividend payout ratio is: cash common dividends/(income before extraordinary items-minority interest—cash preferred dividend) x 100. If this is too much for you, simply use dividends per share ÷ earnings per share as it is almost the same thing. This ratio measures what percent of net income is paid in dividends.

So, if the percent is high, that could be a negative for a given stock, since a dip in revenues, or a spike in expenses (or any other myriad of combinations that lower net income) could make the dividend unsustainable.

That said, if the percent is low, that’s generally perceived as good, since it means the dividend payout is protected against adversity. (Parenthetically, it could be perceived as bad, if the company is holding onto too much cash and depressing shareholder value, which is what hedge fund activists are accusing Apple of doing.)

So, I took a look at the list to find what I call the Über Aristocrats in a nod to Standard & Poor’s Dividend Aristocrat Index. Uber Aristocrats would be those companies that have increased their dividends while decreasing their dividend payout ratio.

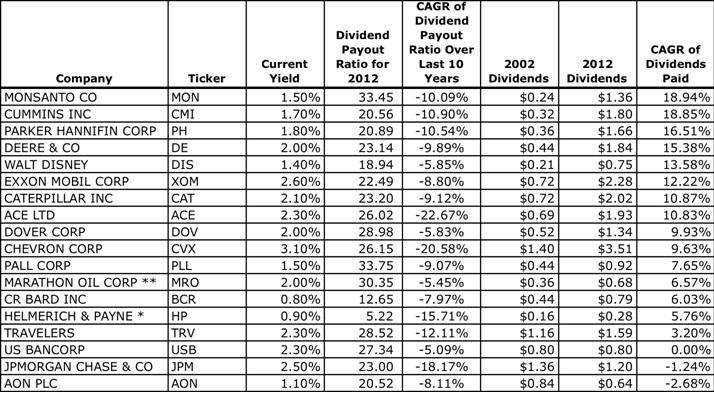

It’s a damn fine trick since in essence the companies doing this are returning ever more cash to shareholders with a decreasing share of the profits. Using a 5% rate of deceleration in the payout ratio as the minimum requirement, the top 18 potential Über Aristocrats were as follows:

I then modified the list a to take into account that being an über dividend payer requires a healthy increase in the dividend payment combined with a decrease in the payout ratio. Taking the above list, and arranging by the largest compound annual growth rate in the cash dividend to the lowest looks like this:

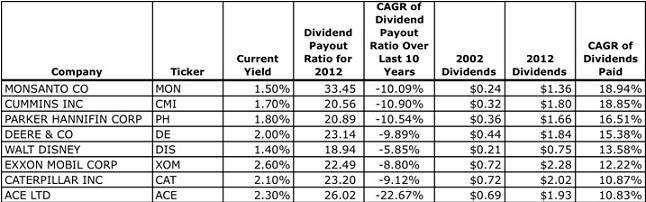

Finally assuming a healthy increase in the cash dividend was double digit compound annual growth, I finally arrived at the Über Aristocrats:

Of these stocks, we own in the Beta Fund Monsanto, Deere, Caterpillar, Disney and Exxon.

Though it might be altogether anticlimactic to mention it, the analysis may not be as neat and tidy as I’ve made look it here. Of the 500 companies in the index, only 133 had complete 10 year dividend data.

While I suspect for many of them, data was incomplete because sometime over the past 10 years they suspended their dividend, I also suspect that mergers, acquisitions and spinoffs (note Altria spun off Kraft and Philip Morris International over the last 10 years) means there are probably several more Über Aristocrats out there waiting to be found.

Nobody ever said the search for value was easy.

Sources: Dividend data: divdata.com, Value Line Publishing, LLC; Payout ratio formula: Bloomberg; Current dividend yields: Capital IQ.