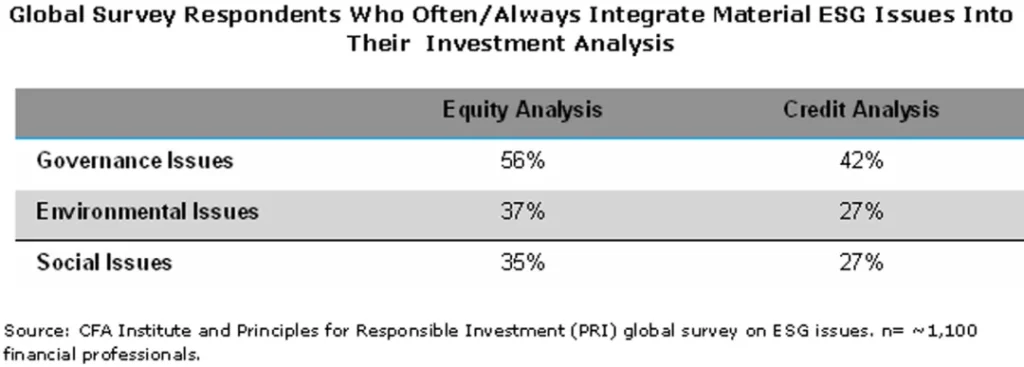

Based on a global survey conducted by the CFA Institute with Principles For Responsible Investment (PRI), equity investors integrate environmental, social and governance standards (ESG) into their analysis more often than their fixed income counterparts.

Remember, so called fixed income investors buy, sell and manage bonds while equity investors buy, sell and manage stocks. Bonds are loans while stocks represent ownership interests. Accordingly, the above statement means that lenders aren’t as concerned about integrating ESG standards into their analyses as much owners do.

This result may not come as a surprise. The first application of responsible investment practices—predominantly divestment and voting practices—were to fundamental equity strategies. ESG integration in equities started gaining momentum at the beginning of the 21st century, while ESG integration in fixed income is still in its infancy, although expanding rapidly. As a result, most asset owners and investment managers look to integrate ESG issues into their equity portfolios and funds before turning to their fixed-income portfolios and funds.

The belated development of ESG integration in fixed income reflects a previously widespread view that ESG integration and fixed income are incompatible, based on arguments such as the following:

- The inherent complexity of bond markets—given the greater size of the market, variety of instrument types, maturities, and issuing entities—makes it harder to integrate ESG issues into credit risk assessments, especially when assessing interest rate risk and liquidity risk.

- Corporate bondholders can’t vote, and find it harder to effectively engage due to limited access to management (bondholders do not have a formal communication process such as the annual general meeting), while sovereign debt holders find it harder to effectively engage with sovereign debt issuers such as governments.

- ESG factors impact bond prices less frequently because: 1) low liquidity in the credit market (especially compared to equity markets) makes it hard to buy or sell bonds based on news of ESG controversies and 2) Interest rates and inflation have the overriding influence on bond prices and therefore it is not necessary to analyze ESG issues.

Changing Views

These views are gradually changing as an increasing number of practitioners incorporate ESG issues into fixed-income portfolios and funds. Of course, fixed-income practitioners still can’t vote, but they do engage.

For instance, portfolio managers and credit analysts regularly contact companies and meet management in person, sometimes with their firm’s equity portfolio managers and equity analysts, and at roadshows. However, it is still rare for a group of fixed-income practitioners to engage with companies collaboratively and for fixed-income practitioners to engage with sovereign debt issuers.

In fixed income, a key application of ESG data is to inform the analysis of issuer creditworthiness. Some practitioners have integrated ESG factors into their interest rate risk analysis when assessing bonds with varying maturities issued by the same issuer. For some issuers, the material ESG factors associated with a five-year bond will differ from those associated with a ten-year bond.

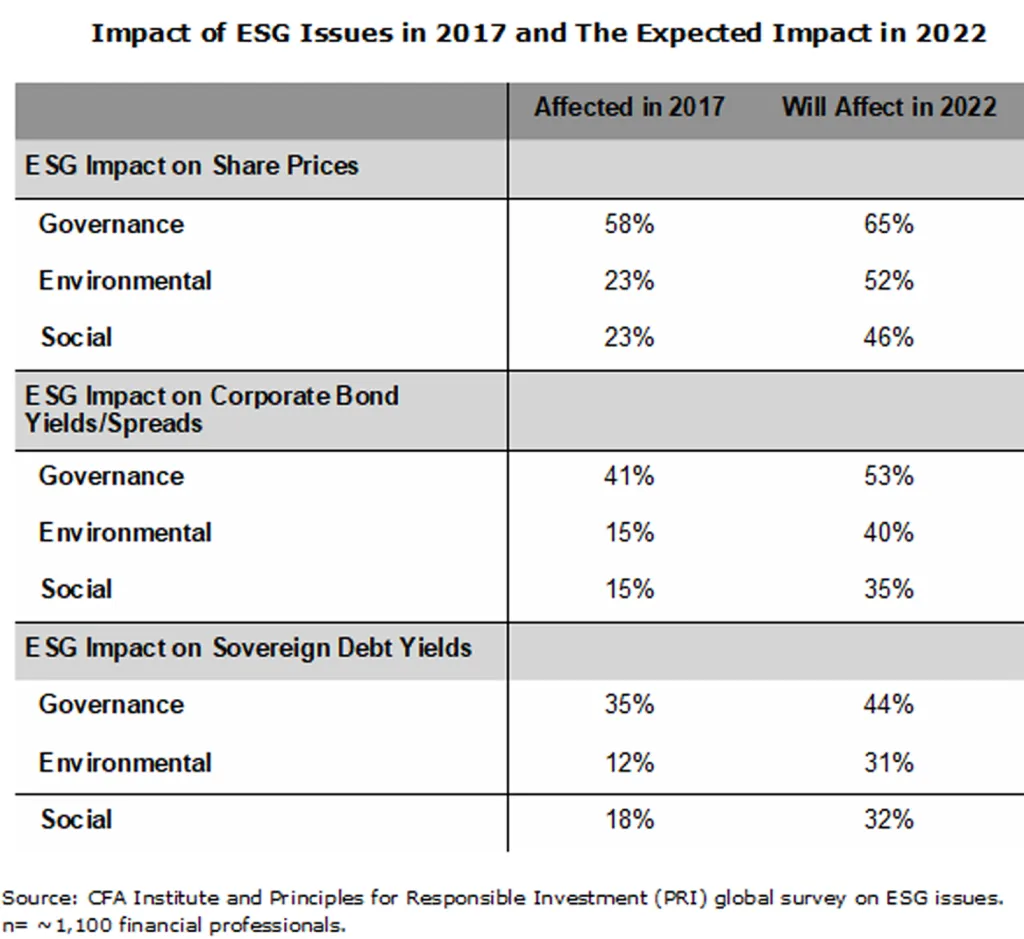

That practitioners are now integrating ESG factors into their fixed-income analysis suggests they do believe that ESG factors can be material and therefore can affect bond returns. The CFA-PRI survey supports this conclusion. The table below shows that survey respondents believe that ESG issues are impacting share prices, corporate bond prices, and sovereign debt prices and will do so even more frequently in five years’ time (2022).

Equity Orientation

The table above also shows that across governance issues, environmental issues, and social issues, practitioners believe that these issues are impacting share prices more often than bond prices. Some arguments that practitioners have used to back these results include the following:

- Share prices are more reactive to news flow and market sentiment than bond prices. When an ESG controversy that impacts a company becomes public knowledge, the effect on the company’s share price is greater than the effect on the company’s bond prices.

- The equity market is more liquid and has higher volatility than the credit market. Thus, ESG factors have a more immediate impact on share prices than bond prices.

- Client demand is higher for equity products with ESG mandates. Therefore, asset flows drive share prices more than bond prices.

- The upside potential of bonds is limited, which can act as a buffer to bond price movements.

- Macroeconomic factors, in particular interest rates, are key drivers of bond prices and override the impact of ESG issues.

- Due to the fixed-income market’s size, variety of instrument types, maturities, capital structure positioning, and issuing entities, ESG factors impacting an issuer may manifest themselves differently depending on the bond characteristics.

When comparing the figures for corporate bonds and sovereign debt, the results suggest that environmental, social, and governance issues impact sovereign debt prices less frequently than corporate bond prices, but only slightly.

Interestingly, social issues are considered to be impacting sovereign debt yields more frequently than environmental issues both in 2017 and in 2022. Social and environmental issues are considered to impact share prices and corporate bond yields/spreads at roughly the same frequency now but by 2022, environmental issues will impact more frequently than social issues.

But stepping back further, the results of the survey offer an important point to consider. Specifically, as ESG analysis takes hold in the credit markets, there is the possibility of leverage in the influence it exerts on corporate decision and policy making. Specifically, by some counts, in the United States, the credit markets are three times the size of the equity markets. As a result, large public companies, private companies, as well as municipalities and foreign governments will soon come under the purview of ESG influences.