The integration of environmental, social and governance (ESG) factors into investment analysis is easy to define. It is the explicit and systematic inclusion of ESG factors in investment analysis and investment decisions.

However, ESG integration in practice is much more difficult to understand. To do so, CFA Institute and Principles for Responsible Investment (PRI) surveyed 1,100 financial professionals, predominantly CFA members, around the world; ran 23 workshops; interviewed practitioners and stakeholders and published more than 30 case studies.

This effort resulted in the publication of Guidance and Case studies for Integration: Equities & Fixed Income by CFA Institute and Principles For Responsible Investment. This work can be seen in its entirety here.

This article concerns our findings with respect to ESG integration for corporate bonds. In subsequent articles I’ll cover ESG integration for municipal bonds, sovereign debt and structured credits.

Parallel Teams

Originally, corporate bond practitioners adapted the materiality/sustainability frameworks and ESG techniques used by the equity practitioners in their firms. This approach still happens and is relevant today.

More recently, ESG integration techniques applied by fixed-income practitioners have become more sophisticated and some practitioners have fully adapted their processes and analysis to integrate ESG factors.

Additional aspects need to be considered when analyzing ESG risks and opportunities in fixed-income investing as compared to equity investing. Bonds come in all shapes and sizes, with differing issuer types, credit quality, duration, payment schedules, embedded options, seniority, currencies, and collateral. Bond prices are strongly influenced by fundamentals, macroeconomic factors, interest rates, and liquidity, which require a multilayered analysis of credit risk, interest rate risk, yield curve risk, and liquidity risk.

All these variables require a sound understanding of how ESG issues can affect a bond. For example, due to the long-term nature of ESG risks, short-dated bonds issued by a company could be investible while the company’s long-dated bonds may not be, if the practitioner perceives that the ESG risk will not materialize within the next five years.

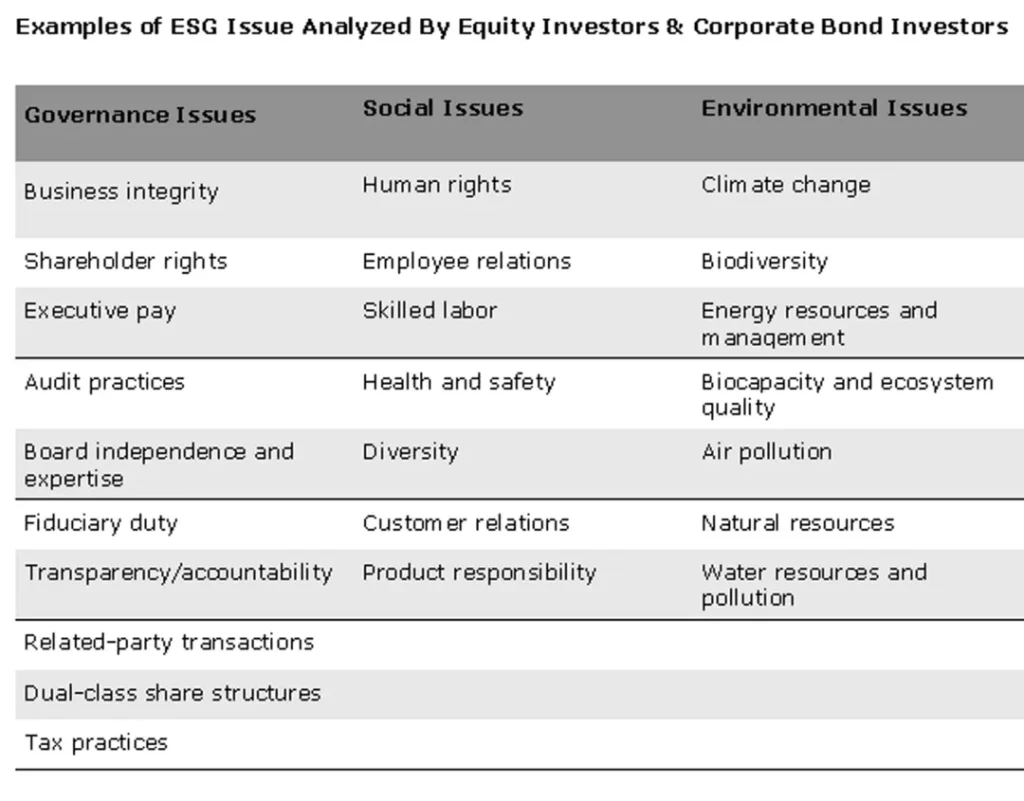

The material ESG issues for a company remain the same regardless of whether the investor is a shareholder or a bondholder. For example, health and safety remains a top ESG issue for mining companies and their owners and lenders. Environmental issues confront energy company owner and lenders while tax practices represent an ESG challenge for multinational companies. See the chart below for examples of ESG issues analyzed by equity and corporate bond investors.

These industry specific issues are reflected in the approach used by some practitioners. Materiality/sustainability frameworks—a regularly reviewed list of sector-specific and/or country-specific ESG issues— are shared by corporate fixed-income practitioners and equity practitioners to identify material ESG issues.

In instances where asset owners and investment managers deploy dedicated ESG teams, fixed-income and equity practitioners share this resource and use the same company ESG research. Other practitioners will adapt the materiality/sustainability frameworks used by equity teams where material issues can be different for corporate bond issuers (e.g., innovation management may be less relevant), especially when considering the duration of bonds.

Incorporating Credit Risk

Practitioners use materiality/sustainability frameworks and company ESG research in their credit risk analysis. Few practitioners have looked at the impact of ESG issues on interest rate risk, yield curve risk, and liquidity risk.

Practitioners assess the impact of ESG issues on a company’s ability to pay its debt obligations and liabilities. Their main approach is to use third-party ESG scores or proprietary ESG scores along with traditional credit analysis when making investment decisions. Some practitioners embed their company ESG research and scores into their internal credit assessments. When they do so, the ESG issues can influence credit assessments and investment decisions.

On a lesser scale, the impact of ESG issues is being quantified by practitioners in portfolio construction processes and fundamental credit analysis. Portfolio construction tools would examine how ESG issues are influencing macroeconomic and market factors. The impact on the portfolio is through the weighting of sectors and companies.

Through fundamental credit analysis, key credit ratios are adjusted for ESG issues. Practitioners assess these ratios to understand whether the creditworthiness of the company is deteriorating or improving and ultimately, to see the potential impact on credit ratings and credit spreads.

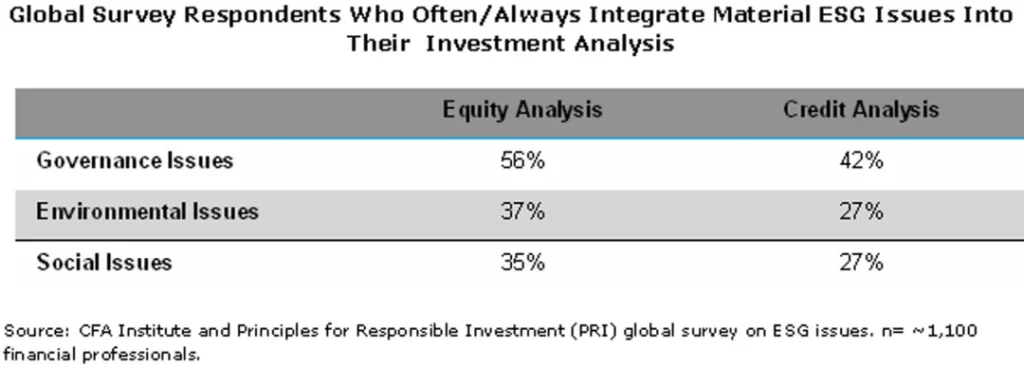

As the table below demonstrates, ESG integration occurs more frequently among equity investors than fixed income investors.

However, given that debt markets are often a multiple, in size, of equity markets, we would anticipate these figures to even out over time in terms of the degre and mix of participation. Key factors which will drive this shift include more and better sources of information, standardization of data and a higher degree of skill and facility among asset managers and other practitioners.