A two-day M&A conference held by Gladstone Associates during the first week of May highlighted the growing influence of private equity investors in the RIA business.

The boutique M&A advisory firm, based in Plymouth Meeting, PA, hosted the event in Atlantic City. Approximately 100 RIA principals from around the country were present, representing approximately $320 billion in assets under management. Participants were looking to grow their business through acquisitions and assessing the market regarding the sale of their own firms.

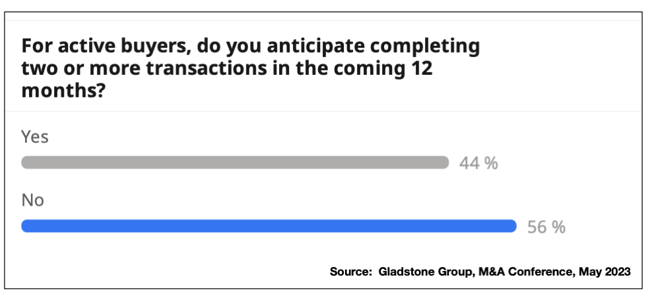

Based on surveys conducted at the conference, just under half, or 45%, of the principals reported they anticipated completing two or more transactions in the coming 12 months.

Buyers and sellers noted the increasingly prominent role private equity capital continues to play in the RIA M&A landscape, which creates advantages and challenges depending on where you sit at the table. According to Daniel Kreuter, chief executive officer of the Gladstone Group, “Private equity investors have definitely raised the table stakes around the pricing for RIAs, which is great news if you own or are building an RIA business.”

Kreuter added that with active private equity investors, aggregators have ample access to capital to build their portfolios.

But on the downside, he noted that at current valuations, the stakes are higher for everyone, particularly RIAs who are looking for growth through acquisitions and may be financing a deal using their balance sheet or borrowing money. “Nobody likes to have a deal go south, but the impact is different for a private equity investor, versus, say a family-owned RIA who might be looking at M&A as a part of their succession planning,” Kreuter said.

According to Derek Bruton, senior managing director of Gladstone, uncertainty regarding enterprise values reflects a confluence of several factors. “The cost of debt capital has increased dramatically over the past 12 months, and unstable conditions in the financial markets have forced buyers to exercise more caution,” he said. Smart buyers, he noted, understand they need to pay more to be competitive. He said, “But they are mindful of their leverage ratios and do not want to cross thresholds that are uncomfortable.”

He added that the presence of private equity buyers has injected some challenges regarding multiples. “P/E firms are well capitalized, and can afford to pay more. But for an operator who’s been in the trenches and knows how the business works, stepping back or being more opportunistic could be the prudent move.”

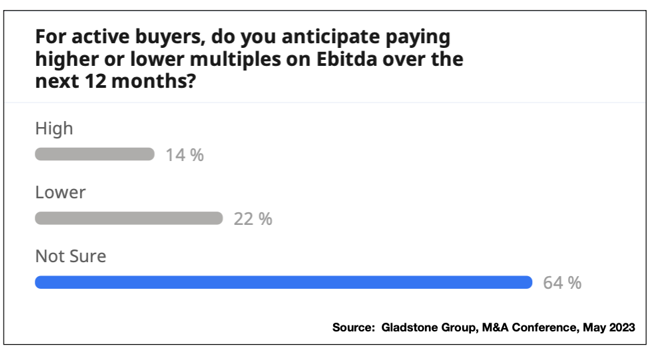

While multiples are higher, a survey of conference participants indicated a great deal of uncertainty:

During an “ask the sellers” panel, Gladstone’s president and moderator, Michael Bilotta, found that principals who stayed on board following the sale of their RIA business generally had a positive experience. Each of the five firms represented on the panel had their RIA’s name and brand subsumed into the brand of the acquirer, and nearly all the management and staff of each joined the new firm. “We’ve had our best year of growth since the transaction,” said Mimi Drake, partner and co-market leader of Cerity Partners. Her former firm, Permit Capital, sold to Cerity, a $40 billion national RIA, in 2022.

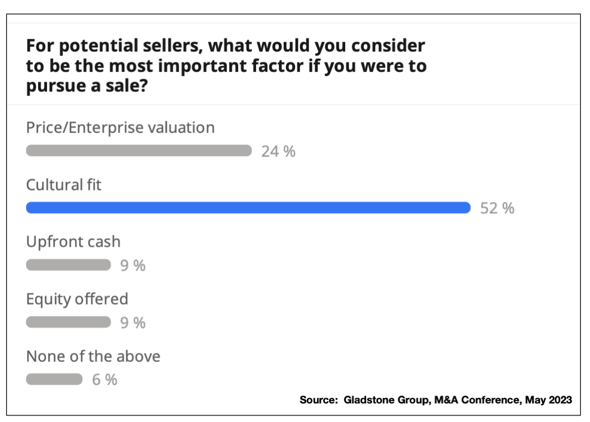

For all the talk about pricing, sellers were primarily concerned with cultural issues when contemplating a sale of their business according to a survey of conference attendees.

The focus on culture is not surprising, according to Bilotta. “While buyers, in particular private equity investors, focus on dollars and cents, the sellers are motivated by a different set of factors. Founders and principals have nurtured their business for years. They have lasting and important bonds with their clients and employees. In this context, valuation matters, but so too, and perhaps equally, does finding a good home where the clients and employees can thrive.”

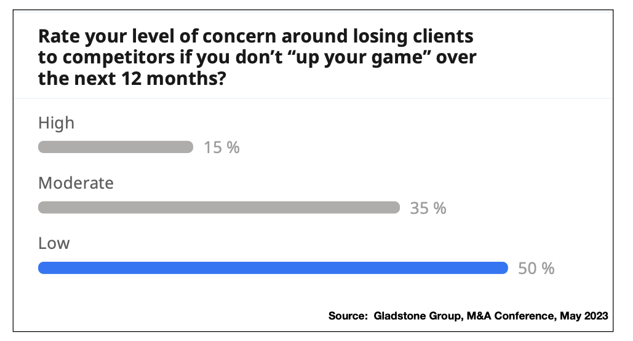

While half of attendees were confident they could compete with their larger peers, the other 50% were not so sure:

“Yes, some advisors want to cash out, and almost all are looking for an able steward of their corporate legacy,” said Kreuter. “But an even bigger interest for these owners is to join forces with a larger firm that has the scale and resources to more readily compete in asset management, financial planning, and marketing and business development.”