David R. Evanson

Forward: I wrote this book for students of business, and maybe students of human nature too.

I say students because, for better or for worse, the people covered in these few short stories, all of them clients, taught me a lot of what I learned on both topics.

It’s a gallery of heros, fools, visionaries and rogues who succeeded and failed on a grand scale. Some operated in the spotlight, but, like most of us, most toiled in relative anonymity.

In each story, I’ve offered up what I learned, but I hope readers will not get too caught up in that. Really, the main goal here is to entertain and amuse.

Table of Contents

The Best Businessmen I Worked For

Owner operators shall inherit the earth.

SmartWater, Before It Got Smart

Underestimate entrepreneurs at your peril.

Mr. Bill

You never forget your first boss.

The Guy Who Invented Paid Search

It’s rarely profitable arriving at the party too early.

At The Urinal, My Career Went Down The Drain

Saying nothing often trumps saying something.

The Catcher in the Lie

If something smells fishy, it probably is.

The Most Successful Guy I Knew

Guts and conviction, not education, builds fortunes.

Wolf Pussy

Be wary of the inventor turned CEO.

The Best Businessmen I Worked For

| Owner operators shall inherit the earth. |

The best, most talented businessmen I worked for lifted an aerospace components business out of an old-line office products company, and built a fortune for shareholders, themselves and the deal’s initial financier, Citicorp Venture Capital.

Rick was the CEO and John was the CFO. In the years following their 1994 initial public offering, the pair orchestrated a string of acquisitions that should be chronicled in business school strategy texts.

In the aerospace business it seems that no matter where you are in the component food chain, there’s a temptation to acquire your suppliers and/or your customers so your company can offer not just parts, but solutions.

What this management team did extremely well was to acquire a lot of related companies with very inexpensive debt. Then they trimmed costs and increased top lines. As the stock rose in response to growing earnings, and reached new, higher ranges, they sold more stock to pay off their debt. The company “reloaded” about three times during the years I worked with them, and today it’s worth billions.

What I thought should get noted in business case studies is that they didn’t just acquire companies portfolio style. They were operators too and got into the guts of things. And they were good. And that meant when the time came to pay off debt with equity, i.e. stock, they minimized the amount of equity that had to be sold.

That’s a big deal because if there’s one thing investors hate, especially institutional investors, are more shareholders diluting their ownership. In terms of minimizing dilution, these guys were heroes.

Of the two, John was so confident of his views, that he was unassailable on any topic that might arise. No point in trying.

Rick was more reserved. At least around me. He knew me well enough though, because we went on the road to meet with investors several times. He liked to poke fun at me in a wry way because I was one of his links to Wall Street and he didn’t like Wall Street.

The most memorable demonstration of his distaste occurred when we were at a transportation conference. I pleaded with him to play the game a little and offer the investors a vision. He replied, “If they want to really understand this company like they say they do, I’m going to give it to them.”

I knew what was coming. He wasn’t going to talk strategy and vision at all. He used his entire 45 minutes to drone on about each subsidiary and what they did: landing gear assemblies, cargo hold tracks, fuselage components and auxiliary power units.

Most executives of companies his size would have broken down the subsidiaries into segments and dispatched with them in 5 minutes. Not Rick. He wasn’t going to kowtow to Harvard flunkies re-arranging debits and credits for a profit. He was making the things that made America great, and by God, they were going to know it.

I never agreed with his views on Wall Street. Every industry has its warts. How many government aerospace contracts ended up in litigation? My view was that Wall Street provided him the capital to do what he did and, absent their particular way of looking at a company, he might not have accomplished anything.

Most entrepreneurs fail when their plan is driven by M&A because M&A is devilishly tricky. So tricky that it’s aptly summed up by the infamous cover of The Economist showing two camels fornicating in the desert under the headline “The Problem With Mergers.”

I had this cover framed and hanging behind my door. When an entrepreneur or an executive told me their plan was to consolidate a fragmented industry through acquisitions, I closed my door to give them some idea of the reception they might get from investors.

Very few entrepreneurs or CEOs get M&A right, and as The Economist suggests, whether they do or not, it’s rarely pretty. But Rick and John got it right but the only case study about their incredible story are these few, inadequate words.

SmartWater, Before It Got Smart

| Underestimate entrepreneurs at your peril. |

At some companies I worked for I got a sliver of equity. Sometimes I asked for it and sometimes it was offered up. The one instance I could have gotten equity and didn’t ask for it would have been worth about $20 million when my client, Energy Brands, Inc. maker of the now ubiquitous SmartWater, was bought by Coca Cola for more than $4 billion.

Equity is nice, but you can’t pay bills with it, not in the present anyway, and at the time, I had a lot of bills.

The other reason I didn’t ask was a lack of faith in the company. Maybe it was how the first working meeting went that gave me the willies. I met them at a law office in Stamford, CT instead of their offices in Whitestone, Queens near the LaGuardia airport.

It turned out the attorney represented my client’s sole supplier of water. Energy Brands was behind on their payables to the tune of $58,000. The water company wasn’t going to pull the plug, but having the meeting in their attorneys office sent an unmistakable message that things needed to get caught up. And soon.

The guy who hired me, Bill, understood all of this. He came to the meeting with a check for about $35,000, then trotted me out as the professional who was writing the plan that would enable Energy Brands to the raise capital that would make them a better and more reliable customer. I didn’t have to say much and I didn’t. All I had to do was show up so that Bill could set his table.

The reason I thought I could have gotten equity if I’d asked, was because the meeting demonstrated relatively small amounts of money were important at the time. After all, if they were holding back $23,000 from the company’s most important vendor, then my fee, about $15,000, was material too. If I’d offered to exchange it for, say a 0.50% equity stake, I think they would have taken it.

Though he took the lead that day, it wasn’t Bill’s company. It was his son’s, Darius. Darius founded the company, and lead it through a series of pivots that were thoughtful and interesting, but did not yield earnings.

Darius was about my age. Usually I got close to the entrepreneurs I worked with and I looked forward to getting to know him. But Darius’ interest in me never rose above blasé.

So, with this chip on my shoulder coming out of the attorneys office, my impression was Dad was coming to the rescue, and that an equity stake in the company was likely going to be worthless. This was not overtly negative. It was borne out of experience. Most equity stakes turned out to be worthless.

Perhaps in particular in this case because we were talking about bottled water.

Overall, water sales were flat. The five gallon containers for offices and factories, and the one gallon jugs sold in supermarkets, which together accounted for something like 90% of total water sales were barely growing. And water’s “share of stomach,” i.e. its’ percent of all liquids consumed annually by the average consumer, hadn’t budged in years.

But against this backdrop, water sold in convenience packaging was red hot and growing exponentially. Suddenly Energy Brands had a story to tell.

Bottled water is ubiquitous today. But back in the early 90s, it was a new phenomenon which rose to prominence following the industrywide success promoting the health benefits with what the beverage industry called new age teas and juices.

I wrote the plan, delivered it, responded to requests for changes, which were minimal. I don’t know what they did with it, but likely raised the capital that got the company to the next level. When I learned they were acquired for more than $4 billion, I calculated the value of my hypothetical stake, shook my head, and kept moving.

Mr. Bill

| You never forget your first boss. |

Bill was foreman at my father’s boat works.

He was an interesting guy too. To me, his face was right out of a Norman Rockwell painting showing America’s backbone: the working man. Squarejawed, clean-shaven and perennially dressed in grey work clothes.

I was introduced to Bill when I was 7 or 8. He was a different kind of man than I was used to, smelled nice and was funny. I developed an enormous affection for him. As I got older, and began working in the yard, my affection for him waned, but my respect never did.

Bill had lots of facets. He was a Jehovah’s Witness, and devout. His lighted-heartedness darkened over the years and his humorous side aded to flashes rather than a defining characteristic. Also, devout beliefs aside, he could conjure up imagery that would make a working girl blanche. I never knew so many everyday objects could get wiped across a pig’s ass, and that once altered, had a new name assigned to it.

He was a family man too, and built his own house on a rural parcel, ultimately boarding my sister’s horse.

Sometimes wincing displays of self-loathing would surface as well. I remember one time we were in a dingy together. A storm was coming, and we were replacing lag bolts on the pilings because several failed during the last storm. I was holding the dinghy steady while he replaced the lag bolts.

And it turns out some of the tops of the pilings were rotted. Looking at them he said, “Yep, there’s shit in there, just like you’d find in my head if you kicked it open.” Wha?

Most of the time though Bill was Bill for his take on what was going on, and depending on your perspective, what was going on was pretty interesting, and scary. This was the 70s. Son of Sam was lurking. Jim Jones was serving Kool-Aid. Pulling the plug on Karen Ann Quinlan’s life support was a national debate. Patty Hearst was brandishing a machine gun in a bank. Then there was the Vietnam War.

And Bill gave his spin on all of it, mostly at lunch time, in short statements, all rapidly delivered in a matter of fact tone. And I think overall, he was disappointed with the way the world was going and deep inside him there was darkness.

I worked for Bill several summers and during school breaks. He gave me just the right amount of crap for being the boss’s son, but never stepped over the line. I think about Bill from time to time, even 50 years later, largely I think because Rockwell got it right.

The Russians Are Coming

| Cultural differences can lead to some of the most rewarding business experiences. |

My client, Boris, was an immigrant from the Soviet Union who came to New York City in 1972 with a wife from an arranged marriage. Boris is not his real name, but the real one is every bit as Russian as Boris.

He got a master’s degree from C.W. Post, and, ironically some of the courses he took were, provisionally, taught at West Point. Mind you, at the time the Soviets were the Evil Empire, an here was Boris, a Soviet sitting among them.

There’s a lot of backstory, but when I caught up with Boris he was CEO of Restart Venture Capital (a play on the firm’s real name), and principally was borrowing money from the federal government on favorable terms to make high yielding loans for taxi cab medallions. At this time, the founder of Uber probably wasn’t even born yet, and taxi medallions were worth a small fortune. There were just 11,500 medallions in a city of more than 10 million, and they were rock solid collateral.

I was part of the team that took Boris public, handling the media and investor relations aspects of the story.

We were close. Not because of the duration/frequency of exposure, but rather, for one reason or another, we understood each other. And we were frank about the realities of the money business in New York City. Whenever I asked him about this or that, invariably he would ask, “Is it good for the Jews?”

If your job was getting exposure in the mainstream business press, Boris was a wet dream. He had all the right handles.

His company was a licensee of the Small Business Administration. He used his license to form a Specialized Small Business Investment Company or an SSBIC. For every dollar he raised privately, he could borrow three more from the SBA on favorable terms.

The Specialized part meant his company, Restart, had to offer loans and make investments in minority owned enterprises. And for distributing capital to minorities, SSBICs could offer their investors something no one else had: the most compelling tax break the IRS code had to offer. The tax break was this: anyone who reinvested capital gains from another investment into an SSBIC could virtually eliminate the taxes owed on their prior capital gains.

Policy wise this was all well and good, but in reality most SSBICs were privately held and investing in them was limited mostly to accredited investors. So as fat as the tax break was, realistically it was not available to most Americans. But when Restart began trading publicly on Nasdaq, the tax break was accessible to just about anyone who wanted to take advantage of it.

With a Soviet immigrant running a venture capital firm parceling out tax breaks on capital gains — any part of which was enough to make deceased Politburo members turn over in their grave — it was a pretty easy pitch to the New York Times. And sure enough, a few weeks after he went public, there was a two page spread in the Sunday New York Times on the life and times of my friend Boris.

As successful as Boris became he remained the same in one respect, summed up by the expression You can take the man out of the Soviet Union . . . So no matter how close you might get to him, no matter how intimate, you never got the full story. He reserved that for himself.

So when I called Boris that Sunday to ask him if he had seen the New York Times article, he told me that he had already put the Times in the trash and would see if he could dig it out later that day. I knew he read it. Whatever. Any emotions he might have had about being the new poster child of capitalism were his and his alone.

Stupid Private Equity Tricks

| Ivy League degrees, bow-ties and white shoe resumes can mask unbridled greed |

I was talking to the vending machine guy in a client’s kitchen. I asked him why he thought his customer had gone from one crappy and regularly abused vending machine, to several vending machines per kitchen on three floors of a suburban office building.

He didn’t know so I told him the 10 fold increase in his business came in large part because a private equity investor bought the company and they had just one mandate: growth.

Additional space was leased, employees were added, marketing budgets expanded, a $250,000 back-up generator was installed to make sure it was a 24/7 operation.

So, just like Mitt Romney said, investments by private equity investors trickle down through the economy.

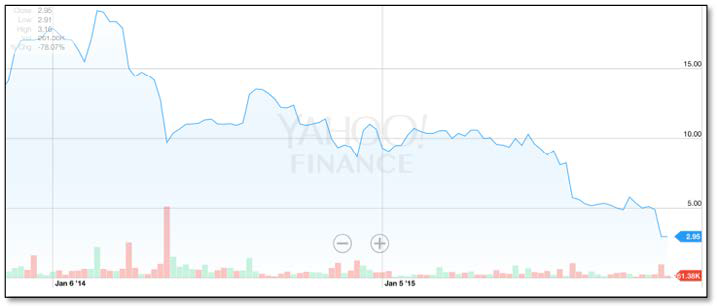

While this company was keeping the vending machine guy happy, the private equity investors were borrowing money, and using it to pay themselves dividends north of $400 million.

Later, the company did an initial public offering underwritten by the whitest of the white shoe investment banks. Below, the price performance chart of the company since it went public.

The loans of $400 million that financed the shareholder dividends, plus another $175 million in loans from an acquisition, meant that at the time of the IPO the interest expense alone was about 35% of revenues. In truth, the distributions the private equity investors received were much higher. Prior borrowings of another $400 million, distributed to shareholders, got wiped out in a bankruptcy filing a few years earlier, and as far as I knew, none of these dividend payments were clawed back.

Most of the IPO shares were bought by institutional investors. Yes, the bow-tied professional guys, who are often fiduciaries for the little guy. Where could they possibly have seen the upside here?

Net, net, more cash went out than came in. While that’s the very purpose of investing, this particular scenario demonstrates how lopsided the ratio can be. Even that might be ok, were it not for the fact that the private equity investor’s gain was ultimately the retail investor’s loss.

It was like the Dutch buying Manhattan for a few trinkets. In this instance, we got Nantucket Nectar and Red Bull and the private equity investors got hundreds of millions. And the IPO investors and the pre-bankruptcy lenders? They got a big fat loss.

The Guy Who Invented Paid Search

| It’s rarely profitable arriving at the party too early. |

I know he invented it, because he did it in 1994, and Google was not founded until 1998.

In 1994, the guy, Jim, didn’t have the Internet. What Jim had was 1-800-Yellowpages.

If you were anywhere in the United States you could call 1-800-Yellowpages and ask the operator where the nearest dry cleaner was, or florist, or convenience store. The thing was, if you were an advertiser with 1-800-Yellowpages, the operator would mention your company first among the choices offered to the caller.

And there it was. Analog yes. But it was still paid search.

The technology that made this service possible was dinner plate sized CD ROMs containing every business and every address in the United States.

Jim’s notion of paid search was ahead of its time. If you use the founding of Google as the start of search, he was about four years too early. Ultimately, 1-800-Yellowpages went up in smoke, leaving a trail of lawsuits in its wake.

It didn’t matter. Right after that, Jim figured out how to use fax technology to target golfers, and soon he was selling them clubs at a rate of $100,000 per day.

At The Urinal, My Career Went Down The Drain

| Saying nothing often trumps saying something. |

All it took was one sentence uttered to a client’s board member who was standing next to me at the urinal.

It was traumatic and scary at the time. I lost everything I had built over the last 20 years.

But from the rear view mirror, it was for the best. I was a very highly paid financial writer and investor relations consultant. While this supported a lifestyle that was likely the envy of 99% of the population, it didn’t make me a nice person. That chapter had to end, and ultimately, I ended it myself.

The board member and I were friendly and, dicks out at a Union League urinal, I said something to the effect that we would need to manage investor expectations with a soon to be reported loss.

I thought about it before saying it. I was an insider and he was an insider by SEC definitions. We were both committed to the success of the company. We were on the same side. We were allowed to talk to each other.

What I hadn’t counted on was the CEO we both reported to hadn’t told the board the company would report a loss.

Of course it’s the CEO’s prerogative to inform the board how and when he saw fit. And apparently that time had not materialized yet. So my untimely comment was a problem.

I might have survived it, but there were other forces at work about to bring this leg of my career to an abrupt end.

Specifically, one of my account executives was having a torrid affair with the company’s chief financial officer, who, of course, was married.

Though she would later turn his life upside down and end a 30 year marriage, at the time, he seemed quite taken with her. And ultimately that was bad for me because something I said to her about him got repeated, presumably during pillow talk, and though he never said anything about it, a massive grudge was born.

So when the unfortunate urinal disclosure came to light, my former partner, and his new partner were immediately called in for a dressing down, the CFO had his knife out. “He’s off of our account as of this moment. What the hell was he doing? Was there some kind of insider trading going on here? Who else was he sharing inside information with?”

Mind you, this was a huge client for us. The monthly retainer was $39,500.

My former partner had his knife out too. We had sold the company about two years earlier. Almost out of the gate, our corporate parent stubbed its toe badly, and sold us to a former Lehman Brothers executive operating a public company engaged in a variety of businesses, the most prominent of which involved contract prison labor.

So when ultimately, and inevitably the time came for us to buy the business back, I was out. I’d had enough. While we were mulling over options, my partner put together a cabal to buy the company behind my back.

Perhaps what the cabal didn’t count on was me doing absolutely nothing about it. So, in addition to the assets, they also acquired my very rich employment contract.

When the dust settled, I was making a lot more than either principal. They let me know that my bonuses, paid quarterly, were coming out of their own pockets. They put income statements in front of me and asked why the cash I was generating wasn’t higher.

So when my former partner got back from his dressing down, it was time for my dressing down. There was a lot of anger. Shame was dispensed. I was asked to write a status update of everything I was working on, and not to report to work on Monday, while the “investigation” was underway.

I never went back. I resigned rather than deal with it anymore. These days I’m pretty careful what I say at the urinal or anywhere else for that matter. Usually I just remark how cold the water is to the guy next to me, and leave it at that.

The Catcher in the Lie

| If something smells fishy, it probably is. |

Whenever I got a referral to write a company’s business plan it was like walking into the unknown. This was before the Internet, so there was no Googling anything. I had to show up to get a good look at the operation.

The first time I walked into Mouli’s office I could smell money, and lots of it. He had a giant Italian-made designer desk devoid of the pens, unopened mail, post-notes, crumbs, and empty Diet Coke bottles that typically populated my desk. There were matching white leather chairs, and chrome and glass end tables.

Mouli was about 30 stories up. The northern wall of his office had a glass window overlooking Central Park. It was fall and the leaves were turning. There were Leroy Neiman paintings on the walls, including one of Mouli himself. His secretary was an exquisitely appointed brunette in high heels who was rumored to be a former Playboy model. He had a napkin tucked into his collar and she was serving him lunch. He looked like a coddled middle schooler home for a holiday.

Just so there are no surprises at the end of this, Mouli’s in jail now, serving out a sentence of 20-plus years. But on the train home after that first meeting, I thought, “Fuck it, I’m not doing this.” Between travel and interviewing his people all day, I had spent 14 hours working for Mouli and did not get paid. The terms of the engagement were clear, and if it’s a problem getting paid on day one, I wasn’t interested in day two.

Of course, when you have nothing to lose you can win. So when I called to say I was out, Mouli was having none of it. I got a check the next day via express mail, and I was back in.

It turned out to be a two year engagement. Originally Mouli was going to distribute “innovative” low tech consumer goods – pince nez glasses, lunch boxes, non aerosol containers and some crazy plastic caps for the tops of soda cans. But technology for video gaming was evolving rapidly. So every time Mouli pivoted away from consumer products, and increasingly toward technology, the business plan had to be updated.

During this time, I met a parade of consultants and employees. The other consultants were getting a bit jumpy because there were a lot of meetings and drafts of things, but nothing much was getting done in terms of moving the business forward. They were also jumpy because Mouli probably owed them a lot of money for their services. I wasn’t as jumpy because I had broken Mouli in with the hissy fit about not getting paid on Day 1.

Regardless, their concerns troubled me and I began to question what was really going on. Yes, I thought something was fishy, but not criminal. He wasn’t selling any securities as far as I knew. He wasn’t even selling any products.

But he seemed to be spending a lot. Worst case I thought, he was helping someone in Israel get money into the United States. Even this theory was strained though, because, in the main, nobody he hired or did business with was affiliated with him. He was blazing his own trail and we were helping him do it.

And ultimately we got him to the doorstep of a reverse merger transaction that would make his company public.

With a deal at hand, the lawyers came in and I was out. As a public entity it was dormant for a while, but then Nolan Bushnell of Atari and Chuck E. Cheese’s fame entered the scene, changed the name of the company, and ultimately, the whole enterprise fell victim to its own madness.

Later, Mouli relocated to California. How he got himself into trouble after that I’m not sure. It wasn’t the line of pince nez eyeglasses that brought him down, and I’m relieved about that.

The Most Successful Guy I Knew

| Guts and conviction, not education, builds fortunes. |

The most successful guy I knew never finished high school. His single academic credential was a GED.

Even though I knew this, there I was at the Lehigh Valley International airport waiting to meet him. He had read my Raising Money column in Entrepreneur magazine. I guess he thought if I knew enough about raising money to write a column, I might know enough to give him some good advice.

I ultimately helped him raise millions and go public, which was not something I did for a living, just something I knew enough about to make happen if pressed. And press me he did. Out of the millions of people who read my columns, this guy was the one person who saw how to monetize my knowledge for his benefit. He was one savvy bugger.

The stretch limo pulled up and the door opened. I didn’t expect the limo. He didn’t get out, but leaned forward so his head and shoulders were perfectly framed in the door opening. “I’m Stephen Kemp,” he said with a smile that looked like trouble. “Get in.”

Stephen was not his real name, but it was like that. Two sharp sounding, but simple words that could be said quickly.

On the way to Manhattan, he lied to his wife over the phone about where he was going. Then he lied to her again about where he was going following the first fictional destination.

He set up meetings in Manhattan with two little investment banks. Little investment banks come in many forms, and these were of the bucket shop variety. Sales assistants were wearing very short shorts with black fishnet stockings and high heels. My guess was the copy room saw a lot of action.

Stephen explained his deal with big spread sheets. His spreadsheets were unlike anything I’d seen. Rather than leading revenues and subtracting expenses to get to net cashflow, he had it upside down. This wasn’t a by product of his limited education, it was a demonstration of how he managed — not to revenues, but to cashflow.

The bankers expressed enthusiasm, but made no commitments. I took it all in, and on the way home explained to him where his approach to selling the deal was problematical, why he did not want to get in bed with the people we just met, and how a round of private capital was the way for him to go. We worked out a consulting arrangement in the back of the limo. He wrote me a check on the spot, the limo came to a stop, I got out and stood in the parking lot dazed and confused.

Over the next few weeks, I revamped his business plan, and worked with him on his presentation. Then I introduced him to a group of private investors I knew who operated in a loose confederacy from a lush suburban office park.

I was curious how these meetings would go, and a little worried too. These guys were not just rich. They all had a social pedigree. There was more than one Winthrop in the bunch, and Stephen was a street thug. On the day of the meeting, Stephen did something that really set me on edge. We stopped in the bathroom before going into the boardroom to make our pitch, and he put his index finger under the tap, put it up to his nose and snorted a few water droplets. Oh my god, was he on coke?

As Stephen made his presentation, the investors must have smelled money, because a commitment to commit was made during the meeting. Wow. We were batting a thousand. Absolutely unheard of.

They did smell money. Stephen ultimately cashed out for nearly $100 million. In the process he made a few of his hometown pals, who might possibly have lived in trailers or grew up in them, multimillionaires.

His big payday masked the utter turmoil it took to get there. And, as time wore on, I got the feeling the chaos emanating from Stephen in ever widening concentric circles was not madness, but a method. He would reinvent until he succeeded.

In a prior incarnation, he used the straight shot Interstate 80 offered into New York City to build inexpensive American dream type homes in Pennsylvania’s Pocono Mountains. It was an integrated operation with a sales company, a land company, a construction company and a mortgage company, coupled with an aggressive sales pitch to working class families about 60 miles east paying exorbitant rents in or near New York City. Why not pay less and own a home where your children can play in the yard?

That company was winding down when Stephen and I met, but the snippets he dropped led me to believe it was a boiler room operation. They roughed up a few customers and the attorney general in New Jersey launched an investigation. Ultimately he and a partner were cleared of any wrongdoing.

So fresh off his controversial success in real estate, Stephen’s schtick was bringing goods and services once reserved for the rich to the masses.

His idea was if this strategy worked in real estate, it would work for breast augmentation. Ninety nine down and $99 a month. Really.

The business was simple. He convinced several cosmetic surgeons to pay him $10,000 per month for which he would deliver $50,000 per month in qualified patients.

But that was just the start of the cash flows. If a qualified patient met with the doctor, and decided to go through with the augmentation, the doctor would offer the patient a payment plan, which in reality was a loan so the customer did not have to put up any cash. That meant saying yes to the procedure was easy.

The loans were typically about $4,500. But then Stephen would buy the loan from the doctor for about $3,800. Since the borrower was paying credit-card interest rates on a $4,500 note that Stephen got for $3800, he was earning more than 38% annually in interest.

Initially, what got the investors juiced was the notion that with a national rollout, earning interest north of 38% on billions of breast augmentation loans was capable of delivering a vast fortune.

Perhaps because the product lay inside the breast of the patient, too many of them seemed to feel if they decided not to pay, there was little anyone could do about it. What were lenders going to do, repossess saline bags at the end of a scalpel? Further, if there was any dissatisfaction with the augmentation, the underlying loan usually went bad.

Everyone anticipated defaults, but the rate was too high and the portfolio went upside down. By this time the company was publicly owned, an added complication to what was quickly becoming a chocolate mess.

Finally, the investors had enough and pulled the plug. It was venture capital. Investor’s didn’t like losing money, but they understood the risks. Yep, everyone was behaving like an adult. And because he didn’t do anything wrong, Stephen got to keep his $250,000 salary until his employment contract expired.

He liked the high life, but a $250,000 salary, even if he didn’t have to work for it, was not going to finance what he had in mind. So Stephen exchanged his salary for the removal of his non compete clause. By then, the investors were done with the breast augmentation business, had no intention of reviving the company and were happy to save $250,000.

He restarted several months later. Same business, different approach. He asked me to be on the board and offered equity as compensation, but I declined. The equity I received for arranging the public offering on the last iteration was at one point worth about $500,000, but ultimately became worthless before I was allowed to sell any.

So I wasn’t too keen to go on another round with Stephen. I lost faith in him. Still, we were friends, had dinner and a few drinks from time to time, and he kept me in the loop. I thought it all had a smoke and mirrors quality to it, but when he sent me the news release from the acquirer, a large and respected public company spelling out the deal in black and white, it was hard to deny Stephen hit it big.

Then I thought about the stake in the company he offered me, and my 21 years of formal education, including a master’s degree in finance. Then I thought about his GED. Then I wondered: if he had as much business training as I did, would this have kept him from achieving the success he did? . . . a question, no doubt, that between us, is only ever considered by me.

Wolf Pussy

| Be wary of the inventor turned CEO |

The CEO was unequivocal in his displeasure: “I don’t know what you’re doing, but to me it sounds like a bunch of fucking wolf pussy.”

Mind you, I had just been flown 4,000 miles to Oakland, California to meet this guy so I could write a business plan for him. I got in late. It was early. I was in a different time zone. We weren’t even past our first cup of coffee. Then the wolf pussy comment, which admittedly, I had never heard before that day.

This was a problem. I had to work with this guy over the next two days to get his story, understand his prospects, and then fly back to New York, write his fucking business plan so Yitz could do a deal for him. I was working for Yitz and Yitz paid pretty well.

After a calming word from the other consultant with us, and then a call from Yitz, who spoke in tones that might be used with a truculent middle schooler, the CEO was brought into compliance and was ready to talk.

This wasn’t much ado about nothing. My guy, the CEO, Jim, had a very cool, very promising commercial product line. What he had, as much as anything could be in 1994, was potentially disruptive.

Jim specialized in photo luminescent crystals. These crystals absorb light, then emit it when it goes dark. What Jim had was technology that kept the crystals glowing long and strong enough that he could offer commercial grade safety products. Exit signs. Floor tiles. Rope for rescue dives. It was cheap and could be used in any building in the world as well as on trains, planes and automobiles. The possibilities were endless.

(He also figured out how to suspend the crystals in water, which unfortunately some foreign security forces used to spray on protesters for later identification. Hey, it was a market.)

What had Yitz and everyone else lathered up was Jim also figured how to suspend photo luminescent crystals in paint. And the other consultant with us, Bob, out of his own initiative, made a huge sale to the owners of the World Trade Center. Following the 1993 attack, some of the lights in the stairways went out. There was vomit that could not be seen by people in the darkened emergency stairwells. Many of the injuries that day came from falls in the hazardous conditions.

Bob convinced the World Trade Center owners that they needed to paint all the stairwells of both towers with photo luminescent paint. That way, the next time the lights went out, the stairway would remain lit. Fewer slips, fewer falls.

Interestingly, Bob actually owned a leather importing business and had his company in the Empire State Building no less. But for whatever reason he needed to make more money, so he was also a marketing consultant, and apparently a paint salesman too. I met Bob because he was consulting to Mouli. I was also consulting to Mouli, so we frequently had lunch together. Often after we were done with Mouli for the day, we stopped at the Yale Club then headed out to some of Manhattan’s clubbier watering holes.

The initial rough patch in that first meeting with Jim stemmed largely from the fact that he wasn’t really a CEO. He was a scientist running a company. His wife told me whenever she hung up his coat in the evening that crystals on the sleeves and elbows glowed gently.

Ultimately he warmed to the process of developing a business plan, and to me too. He had a big, soft underbelly and somehow I made it feel good. At the end of two days, Bob, Jim and I were fast friends and we planned a lush, manly golf outing after Yitz got the deal done.

But most deals never get done and Jim’s was no exception. I think his company eventually faded, but somewhere, I’m sure some of his products are still glowing.

The Math Department’s Worst Student

| Students are in no position to judge the relevancy of what they are learning. |

I was probably the worst math student in the department when I was at Denison University from 1978 to 1982.

My high school career was poor to middling and I felt completing a math major, in addition to an econ major would cleanse my past.

I started all the way back at pre-calc, and as I worked my way up, my GPA went down. Happily whatever math skills gained through osmosis enabled a ~4.0 in economics.

Still, at the mathematics building it was bad. I remember getting a 23 on a statistics exam . . . My GPA in math was below 3.0, but how much further I didn’t want to know . . . Taking actuarial tests twice, once in Scotland no less, where actuarial science was invented, and once in Philadelphia, where I lived, I failed miserably both times . . . Professors contacted for a graduate school recommendation couldn’t even remember me.

Unfortunately if anyone told me how often gainful employment rested upon, in one respect or another, the GPA in one’s major, I might have rethought the math major strategy.

But the student is in no position to judge when their lessons might become relevant.

About four months after graduation I got a job in publishing. It involved reading a lot of prospectuses, and knowing how to do the basic algebra that was required probably got me the job.

Later in graduate business school, having quantitative skills eased my way and provided a significant competitive advantage over other students, some of whom were inumerate.

I parleyed my publishing experience into a career as a financial writer for the media and for corporations. Because I knew math, I had chops, or at least my clients thought I did.

Still, by the standard of a real mathematician, I used little real math. Working with financial statements was important – and yes these statements had numbers – but the required skill was understanding them well enough to draw and expound upon well founded (or at the very least tenable) inferences.

At that juncture, math wasn’t so much a skillset as a mindset. It was the discipline that enabled me to organize words into sentences into paragraphs into complete works all with, as I like to tell myself, numerical order and precision.

Now, today, as a financial writer and a media relations consultant, the stars have finally aligned, at least as it concerns why my focus on mathematics in college turned out right.

That’s because writing is no longer just scribing away. Writing is writing, yes, but a big part of the job is also trying to figure out the social media platforms to project it onto and how. And all the data those platforms send back to me I can analyze and act upon in a way few can – at least few of the people I write for, where my point of contact is likely to have very little in the way of numerical skills. In the end this skill might account for whatever success I’ve enjoyed lately.

With respect to consulting on the media, the surest way to get a client exposure, whether it’s CNBC, or Bloomberg or The Wall Street Journal or the New York Times, is to develop statistically valid surveys. With all of this Big Data coming out of clients’ operations, this is easy. Easy that is if you understand statistics, sample sizes, linear and (admittedly, only on rare occasions) multivariate regression analysis as well as Analysis of Variance or ANOVA.

A math degree even helps with statistically invalid surveys, because if you can explain the shortcomings of what you are presenting to a reporter or producer based on the underlying math, they feel informed well enough to use it anyway.

In addition to my grade point average in math, the other thing I don’t want to think about is how much math I’ve forgotten since 1982. I’ll say this: my understanding of the math I do remember has grown, attributable to mulling it over for about 35 years, generally in the pursuit of suburban labors such as cutting the grass or shoveling the driveway.

It may be altogether anti climactic to mention it, but a simple math problem apparently vexed the university’s development office, and has largely kept me out of their sites. In 2008, I was asked to teach entrepreneurship for a day during January term. The appointment put me on the radar of development and I told them this: Tell me the differential in my tuition as a result of contributions from the endowment, compounded with a profitable rate of interest since graduation, and I would pay them that amount.

It’s been a while since graduation, and it’s probably a big number now. Ultimately, I’ll likely have to use a payment plan to make good on my school’s investment.