The best alternative to venture capital funding is almost never discussed and used even less. This alternative is royalty financing.

Royalty financing is simple. Here’s how it works: You, the investor, advance me, the entrepreneur $1 million. (Note the word advance. More on that later.) I put the $1 million to work and promise to pay you 3% (or 5% or 2% — pick a number) of my gross sales until you get back $3 million — your initial $1 million, plus $2 million more.

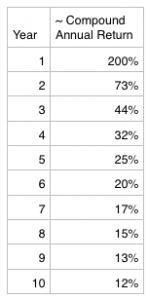

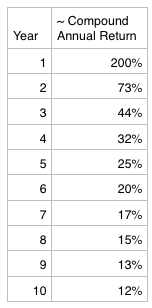

The total $3 million in cash that flows back to the investor rests on reaching a cumulative sales threshold of $100 million, a big number, but not an outsized target for any early stage company where the founders are all in.

Also noteworthy: If my sales mushroom and reach $100 million in one year, your return is 200%. If it takes me 10 years to reach aggregate sales of $100 million, your return is 11.6%, compounded annually. Probably not the kind of return any venture investor is looking for per se, but certainly not anywhere close to the typical worst case scenario. Below, returns for the numbers used in this example:

{kind=link}

For entrepreneurs there’s several benefits to royalty financing.

First, preservation of equity. Sure there are equity kickers that can be thrown in, but royalty financing can eliminate double digit dilution that can and do occur early in the game.

Second, a royalty payment is not fixed, but floats to sales instead. In earlier stage scenarios, fixed obligations against the backdrop of uneven revenues can be a death knell.

Third, royalty financing can enlarge to pool of likely investors. For most companies, the requirement to focus on accredited investors makes raising capital much more difficult. Further, even many accredited investors shy away from earlier stage deals because there’s no liquidity. But the prospect of monthly or quarterly cashflow opens up the pool of prospects. Further, as royalty financing is clearly not an equity offering, the accredited investor requirement may disappear altogether, enlarging the pool of likely investors even further.

In a related note, avoiding an equity offering can reduce the legal and accounting fees for a deal, to say nothing of the angst. Further there’s some precedent to suggest that royalty financing is not even a loan. Specifically, litigation advance firms who provide plaintiffs with funds to plaintiffs before their case is settled use non recourse features and the concept of advancing funds to successfully avoid usury laws.

Royalty financing won’t work for for everyone. For companies that are more than one round of financing away from product sales will find a royalty deal a tough sale. Companies operating in markets where pricing is elastic should not consider royalty financing. Examples: restaurants, distributors.

Royalty financing will work best for companies with products and services where there’s a big fat operating margin that can absorb a 3% price increase. It’s also going to work for company founders who want to raise capital fairly quickly without the dilution associated with traditional, equity driven venture financing.