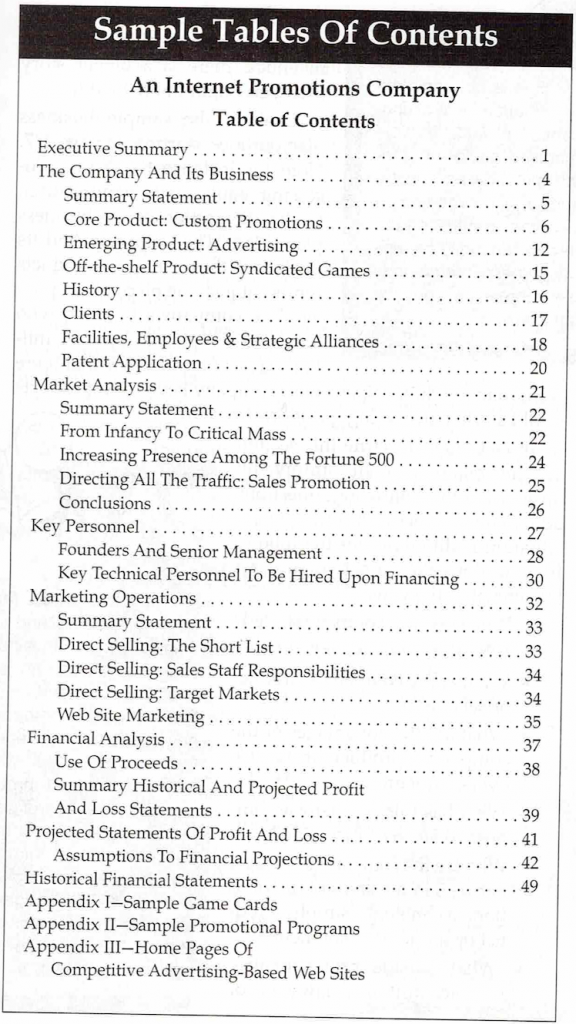

Table of Contents

Planning for Raising Equity Capital

Alternatives to an IPO – Reverse Mergers

Community Loan Development Funds

How To Prepare a Loan Request

How Investors Use Your Financial Statements

Planning for Raising Equity Capital

GETTING STARTED

Most new business ideas are viable. Yet most new businesses fail. Many fail because the entrepreneur does not execute the idea properly. Others fail for want of capital. There are two primary reasons businesses fail to raise the capital they need.

• The entrepreneur pursues the wrong sources of capital

• The entrepreneur fails to adequately plan for their search for capital.

The dictum “Ready, Fire, Aim”, unfortunately, is a formula for disaster when it comes to raising money. Chiefly this is because, for most companies, there are in truth, very few viable investor candidates, and getting in front of one ill-prepared — even though he or she is the one — dramatically increases the likelihood that they will pass on your deal.

| Don’t Forget: You must take the time and effort to plan your strategy. If you are starting a business, or raising money for one in its very early stages, you may only get one opportunity to raise money. Failure to raise capital may mean the failure of the business. |

The following paragraphs offer an algorithm for planning and meeting with angel investors. But in truth, it applies to any equity investor including institutional venture capitalists, investment bankers, and reverse merger candidates.

At the broad-brush level, the sequence of your tactics for raising equity capital is as follows.

• Business Planning. A big part of business planning means writing a business plan. This is fundamental to your search for reasons discussed below. But on a pragmatic level, you can’t set appointments until would-be investors have had a chance to look over your business plan. (See Chapter XX for strategies about writing a business plan.)

• Lead generation. You must find the kind of people who typically invest in early-stage deals. Once you learn where they are, you must qualify them.

• Follow-up, follow-up, follow-up.

• Closing.

BUSINESS PLANNING

Here are the planning steps to follow even before you make that first phone call to investors.

• Prepare a Business Plan. You must have a business plan for two very good reasons. First, if your initial contact with an investor is successful, he or she will request one. When an investor asks to see a plan, or even a plan summary, it needs to be on his or her desk the very next morning. At the very least it needs to go out first class mail, that day. If there is a delay of say three to six weeks between the request for a plan and its arrival, you can pretty much kiss that investor goodbye.

Second, investors ask a lot of questions. Seemingly, that’s all they do. And it’s only by writing a business plan that you can possibly hope to answer the kinds of questions that an investor will ask with the kind of conviction and authority which will win the day. Remember, there is not an entrepreneur on the face of this earth who raised a single penny simply by writing a business plan. They raised money by presenting their plan and using the thinking that went into its writing to defend their ideas, strategies, and tactics before investors. Flip ahead to the chapter titled Preparing a Business Plan (Add link) which discusses how to write a business plan.

| Taking Action: Consider using off-the-shelf business plan software. These programs can stimulate your thinking by confronting you with the kinds of questions which an investor would ask. |

• Determine Your Sizzle. The business plan is the steak. Now, what is the sizzle? What is the one-line answer to the first question the investor will ask: “What does your business do?” The response must be brief, understandable, and memorable.

For instance, if your business resells deep discount travel packages for unused vacations at luxury resorts to Fortune 1000 consumer products companies to use as fulfillment premiums, don’t say that. The investor’s eyes will start to glaze over at the word “unused.” Say: We are the business that makes luxury travel affordable for 50 million middle-income Americans. Then the investor will say “I see,” giving you the opportunity to say “Travel in the U.S. is a $60 billion market annually. With a market this size, there’s lots of niches, and we are operating in one of them which has little competition, and high margins . . . ”

Or, let’s say that your business offers marketing services to physicians for elective surgical procedures, which helps them overcome the ceilings on fees imposed by HMOs and other third-party payors. Don’t say that right out of the box. Instead say, “We are the new breed of marketing agency that every physician in the U.S. now knows that he or she needs if they hope to survive the changes in medicine . . .”

Statements such as these are your sizzle. They are succinct, memorable, and perhaps most importantly, repeatable. You want a sound bite which an investor can easily repeat to his or her fellow investors. Even Wall Street uses this trick. When venerable motorcycle maker Harley-Davidson went public, the pitch to investors was “Own a piece of an American icon.”

• Form an advisory board. Every industry has people who have succeeded. Reach out to these people and ask for their help in the form of serving on an advisory board. There’s a lot of psychology in why people readily agree to such a proposition. Many appreciate being recognized as a success. Others have that natural mentoring orientation which comes from being a successful businessperson. Some want to relive their previous success, while others would simply like to be part of a support system they wish they had when starting out.

But one of the true purposes of forming an advisory board is to help generate leads. When you start asking advisory board members about sources of financing, you will find that many willingly open up their Rolodex’s if they have been properly initiated. To a lesser extent, the purpose of forming an advisory board is to increase the comfort outside investors have with your team.

• Focus On Getting A “Lead” Investor. If you are raising equity capital privately, there’s little likelihood that you will run into one sugar daddy who will cut a check for the entire deal. It could happen, but it probably won’t. More likely, however, you will run into a lot of investors who will put in smaller amounts. These are helpful, but they should be found later. Initially, you need to focus all of your energy on finding the investor or investors who will take down 25% to 50% of your deal, and who by doing so, will provide a magnet for the smaller investors.

| Shop Talk: Investors and entrepreneurs often talk about the “lead investor.” This is the person or institution that makes the most significant financial contribution to the deal. Also, because a large investment by one entity can often attract other dollars, the lead investor is the one which is found first. |

• Seek Legal Counsel. Soliciting capital may provoke several state and federal securities laws. You do not want to unwittingly run afoul of these laws, an act which may cause you to return capital which you worked so hard to raise. Even though many deals are exempt from state and federal securities laws, there can still be a host of requirements on notification, documentation, and the number of investors who can participate in the offering. Raising money is hard. Don’t make it harder by unknowingly breaking the law.

| Don’t Forget: Investors are people too. In order to get a deal done, you must be able to move beyond the language of attorneys and accountants in your presentation, and provoke imagination and curiosity. |

• Prepare a Deal Summary. Technically, this should be the executive summary of your business plan. As mentioned in the chapter about business plans, the executive summary should be no longer than two pages, and must function as a stand-alone document. This summary must describe: the company, the product or service, the market, competition, key personnel, funding required, use of proceeds, and a historical and projected financial snapshot. To stay within the one to two-page length, you should write no more than one paragraph about each of these items.

• Get Referrals. If an investor is interested in learning more about your business after the first telephone call or meeting, he or she might want to talk to someone else such as a customer, a licensee, a franchisee, your accountant, attorney, or members of your advisory board or board of directors. Plan for this question by figuring out who should and will talk. That way, when an investor asks to speak with someone you can answer with a name and a phone number rather than by saying “I’ll get back to you on that.” Remember, you may never get the investor back on the telephone again. Whereas, if he or she is provided with an action step and takes it, the mating dance is still on track.

• Get Introductions. If your lead generation process turns up investors you do not know, then you must work ahead of time to get some kind of warm-body introductions. The best kinds are when someone calls ahead of you and warns you will call. When this happens, you will be able to have an initial telephone call with the investor nearly 100% of the time.

As a fallback, during the first conversation if you can say in your first breath “Our mutual acquaintance Peggy Bennett suggested contacting you . . . ” then your chances of the call being successful, that is the investor agreeing to look at something you send them, increase dramatically.

Former employees, trade associations, accountants, lawyers, or the person who supplied you the lead in the first place, all represent viable candidates to prepare the investor for your initial contact.

• Meeting Venues. If you have something in your factory or office worth seeing, such as people actually doing something, or products being made, then you should always try to get the investor on your turf for the first meeting. However, if you work in a hovel or at home, it may not be a good idea to let the investor see your space. If this is the case plan ahead of time a variety of places you can meet where you know what’s going on, such as the office of your accountant, or attorney, or hotel lobbies which you have been in and which can accommodate an intimate conversation.

| Taking Action: One technique that is sometimes used by companies raising money is the publication of a regular newsletter. This keeps investors and potential investors up on the company as it makes progress. |

LEAD GENERATION

If you ever trace your life’s path in total, you may see that where you have ended up, is to a great extent, the result of chance meetings and random events. The same theory can apply to raising money. You just never know who you will meet who will put you in touch with the person who will be your investor.

Here are some real life examples of such serendipity:

A turkey restaurant owner looking to expand, gets a referral, of all places, from the person who supplied him with ham (clearly not a major vendor) to a franchise development consultant. After that, it was almost biblical in the chain of names that led to the almighty investment capital. The franchise developer, named Bloomenthal had a friend by the name of Levine, who had a friend by the name of Rosen, who had a friend by the name Erlich, who had a friend by the name of Freidman, who knew a merchant banker named Miller, who did the deal.

Or consider this one. The president of a home-based care management company who had been raising money gets the opportunity to make a presentation before an angel investor group. There are some 80 investors in the room; a target-rich environment. His company was met by the investors with all of the enthusiasm normally reserved for a blood test. But a funny thing happened. Prior to going “on stage” the entrepreneur was put in an anteroom with two other entrepreneurs scheduled to present that day. The entrepreneurs started comparing notes and swapping the names of investors they had met. Our health care entrepreneur diligently follows up on these leads, and among them finds his lead investor who commits $200,000 to his company.

Raising money is a lot like finding a job. You must network, network, network. Every person you meet, you need to ask for three more names. One entrepreneur who had diligently saved the business cards of every person he had met over the years sent each one a letter asking for their help in raising money or getting him in touch with investors. He got five investors this way, and a lot of encouragement for what he was doing.

If you are not such a pack rat, here are several paths you can take to start meeting investors. Many of these are described in greater detail in chapter 11, about angel investors.

• Venture capital forums

• Fund-raising seminars

• Venture capital fairs

• Venture capital clubs

• Private capital networks (See Chapter 12)

• Ace-Net (See Chapter 12)

• Professional services firms such as accountants and attorneys

| A Good Deal: Several electronic matching services such as ACE-Net, among others, provide quick and direct access to angel investors. These matching services may not lead you directly to capital right away, but they clearly have the power to start you digging in the right vein. (See Chapter XX – The Internet & Other Electronic Matching Services) |

MAKING CONTACT & FOLLOWING UP

Now it’s time to dial for dollars. Prior to picking up the telephone, you should have put together a business plan and (where possible) gotten some kind of entree to each of the investors you are going to approach. Now you must:

• Qualify The Investor. Your first task is to qualify your would-be investor. This must be done very early on in the process. After all, every investor has parameters and preferences, and if you don’t fit within them, you should probably spend your time on other potential investors.

The investor will ask you very early on in your first conversation who you are and what your company does, to which you should respond, “We are the business that makes luxury travel affordable for 50 million middle-income Americans.”

Then you might suggest some overall industry trends, but then you’ll need to pop the question: “Do you typically invest in companies such as ours?” If the person you are talking to doesn’t invest in companies like yours it’s time to gracefully bow out and move on. But remember, get three more names before you do.

• Answer Questions. If the investor has any interest, he or she will ask a lot of questions. This is where writing a good business plan pays off. Because you’ve thought every aspect of the business through, you should be able to manage these questions.

It’s important, however, to exude confidence and momentum in your answers. The investor is evaluating you from the moment the conversation begins. Equity investors are not like lenders in this regard. They are not relying on cash flows to get their investment back. They are instead relying on you, the entrepreneur, to build value and keep selling the business to other investors until the point where it gets sold to the public or another corporation. The upshot is, if you can’t be convincing to this investor, he or she is thinking you probably can’t convince the next investor down the road, and that ultimately, their investment will remain trapped inside the company.

The reason you want to show momentum is because you want to leave the investor with the feeling that things are happening quickly; that if he or she invested, their money would go to productive use right away, and not sit around in limbo while you figure out the nuances of getting the business to its next stage of development.

• Get A Meeting. Your objective during the initial contact is to get a meeting with the investor. If your list of potential investors is well qualified, meetings will come easily. If not, then getting an investor to agree to a meeting will be more challenging.

Generally speaking, if the investor is interested in meeting, they will request more information, such as a business plan or business plan summary. Don’t agree to sending it out without getting something in return. Specifically, you want the investor to agree to meeting on a certain date after they have reviewed the plan.

Now it’s up to you to make sure your business plan arrives on the investor’s desk the very next day. In addition, as practical, you want to include some kind of sample or tangible evidence of your product or service. If you sell imported, shelf-stable food products, this is easy. If you manufacture waterbeds, this is more difficult. Even in difficult situations, it’s worth considering creative solutions. Pictures, customer testimonials, videotapes among other items can sometimes help bring a product or service to life. Anyone can send a bunch of papers in the mail that pile up on someone’s desk. But product or service samples get picked up, toyed with, and considered.

• Managing Objections. Typically, seeking the first meeting is when you will run into the first wall of objections. “The product is not developed enough,” “The distribution channel is too crowded,” “Your management team is too thin,” “It doesn’t appear that you have established technical feasibility.”

If the investor is qualified to participate in your offering, then you’ve got to be tenacious at this point. Most of the time, when investors decline an opportunity, it’s because they don’t understand a certain aspect of the product, or the market or the technology, or your vision for the company. As a result, when an investor says no, they don’t want to meet, you’ve got to ask them why, and then show them where their thinking is off.

• Prepare a Formal Presentation. You cannot meet with an investor without having a formal presentation prepared. It may not get used, but better to need not have, because if you need it and don’t have it, you’re sunk. Remember, the investor is evaluating your ability to keep selling the company because it’s how he or she will eventually get their return. If you show incompetence in this arena, even if the company shows a lot of promise, it spells trouble for your capital formation efforts.

| AFTER YOUR FOOT IS IN THE DOOR The 20 minute pitch is standard operating procedure; you must be able to tell your story in this period of time. The underpinning of the presentation is your business plan. Thus in the time allotted you must cover the major sections of the plan. Overall you are trying to answer these questions in the investor’s mind: • What is the company and its strengths? • How has it performed? • Where is it going? • How is it going to get there? • What does it mean to me if they succeed? Whether you are meeting with one investor or a roomful, the best strategy is to walk them through a set of 10 to 15 slides, which punctuate your remarks. |

• Conducting The Initial Meeting. There are two very straightforward objectives for the first meeting. First, get the investor to like you. Second, get a second meeting. Entrepreneurs must have two objectives for their initial meeting with the investor. First, get the investor to like you. Second, get the investor to commit to doing some kind of action step.

You must get the investor to like you for a very simple reason. If he or she doesn’t, there’s very little chance that the deal you are proposing will ever happen. Unlike a lender, who bases his or her decision on credit quality exclusively, an equity investor is looking for some sort of personal chemistry, at least for earlier stage offerings. Without some baseline affinity for the entrepreneur and what he or she is doing, there is no basis for an investment. Also remember, that an equity investor can get romanced by business ideas and people, it’s unlikely a lender would change their lending criteria a single iota simply because he or she happened to like the entrepreneur.

But you must do more than simply have the investor like you. The meeting must close with some sort of action step on the part of the investor.

| BECAUSE WE LIKE YOU Getting other people to like you is the subject of another self-help book. But here are the concepts outlined in Part Two of perhaps the greatest book on the subject ever written on the subject How to Win Friends (Simon & Schuster) and Influence People, by Dale Carnegie. Read them over several times before you meet with a prospective investor. • Become genuinely interested in other people. • Smile. • Remember that a person’s name is to that person the sweetest and most important sound in any language. • Be a good listener. Encourage others to talk about themselves. • Talk in terms of the other person’s interests. • Make the other person feel important — and do it sincerely. |

Finally, keep in mind that just like the initial telephone conversation, you want to avoid ceding control of the process to the investor. Therefore, try to make the action steps conditional upon a second, and hopefully closing meeting. For instance: “So you agree to try our product for two weeks, and then meet with me to discuss your thoughts.”

CLOSING

If things have gone according to plan, the date for the second meeting should have been set during the first. But if not, getting this second meeting might take some effort, and a bit of follow-up.

Regardless, the second meeting is deal time. And even if it’s not deal time, it’s certainly the time to separate out the investors who are not worth your time to pursue any longer.

You must pop the question in a way that gets the investor involved in the decision-making process. Also, you must pop it in a way that forces the investor to declare their interest or lack thereof. Here is, in sample dialog form, how to do it:

Entrepreneur: We have met twice. I appreciate the time you have taken to understand my company. Now that you know a little more, and you clearly have some experience in these matters, I want to ask you an important question.

How much capital do you think we should be raising?

Investor: Well, to tell you the truth, I’m glad you asked that. Because I have studied your plan, and I think that you are going to need much more than the $500,000 you are looking for. I think you need $750,000. Not right away, but shortly after you commence marketing — which according to this plan could happen at the end of this year.

Entrepreneur: It’s comments like that that let me know I’ve chosen the right course of action by seeking out hands-on investors, who can provide not just capital but input. Ok, of that amount, $750,000, how much can you commit to?

Gotcha! At this point, the investor has very few courses of action. He or she can suggest a material amount, a small amount, or no amount. If the answer is none, you can say goodbye to that investor and move on. If it’s a small amount, you can solidify this investor’s interest by telling them you are looking for a lead investor and asking them if they will commit the dollars they just suggested when this investor is found. Most will say yes. If the answer is a large amount, then you have accomplished your objective of finding a lead investor.

Getting from a yes to actual dollars in the bank is beyond the scope of this work. However, if you have gotten this far in the fundraising process, you should have had at least some experience with an attorney who has significant experience in securities law. You will now need their counsel in drawing up the necessary subscription documentation, or understanding the securities laws exemptions you are taking advantage of.

| Taking Action: Here are five steps to suggest the investor take after the close of the initial meeting. Have the investor: 1. Read your business plan (assuming they have only read a summary to date). 2. Try your product or service. 3. Speak with one of your references. 4. Have his or her attorney or accountant call you. 5. Call someone he or she has worked with in the past that understands your industry. |

Angel Investors

| CAPITAL FROM ANGEL INVESTORS Definition or Explanation: Venture capital from individual investors. These investors look for companies which exhibit high growth prospects or have a synergy with their own business or compete in an industry in which they succeeded. Appropriate For: Early stage companies with no revenues to established companies with sales and earnings. Companies seeking equity capital from angel investors must welcome the outside ownership, and perhaps the surrender of some control. In addition, to successfully accommodate angel investors, a company must be able to provide an “exit” to these investors in the form of an eventual public offering or buyout from a larger firm. Supply: The supply of angel investors is large within 150 mile radius of metropolitan areas. The more technology driven an area’s economy is, the more abundant these investors are. According to Jeffrey Sohl, director of the Center for Venture Research at the University of New Hampshire, America’s 250,000 angel investors pump some $25 billion to $30 billion into growing businesses, each year. Best Use: Runs the gamut from companies developing a product to those with an established product or service, that need additional funding to execute some marketing program. Also, for companies that have increasing product or service sales and need additional capital to bridge the gap between the sale and the receipt of funds from the customer. Cost: Expensive. Capital from angel investors will likely cost no less than 10% of a company’s equity, and for very early stage companies perhaps more than 50%. In addition, many angel investors will charge some sort of management fee, in the form of a monthly retainer. Ease of Acquisition: Angels are easy to find but sometimes difficult to negotiate with, because they usually do not invest in concert, and may demand different terms. Range of Funds Typically Available: $300,000 to $5 million. |

WHY ANGELS?

For most small or new businesses, so-called angel investors are the most appropriate source of financing. There are many reasons for this. Some of the more fundamental and important:

• Angel investors are one of the most abundant sources of capital in the U.S. America’s 250,000 angels invest $25 to $30 billion each year in growing businesses.

• Angel investors typically provide equity capital. For most emerging businesses, equity capital is appropriate, because it is permanent, and does not require monthly or quarterly interest payments.

• Angel investors will typically invest in a business for reasons other than economic. A desire to help young entrepreneurs, and fill the role of the mentor they never had, is a reason frequently cited by angels about why they invest.

• The amount of capital that emerging businesses need, generally from $250,000 to $5 million matches the commitments which angels typically make.

| Shop Talk: The term angel investor derives its origin from Broadway. The wealthy individuals who typically financed lavish productions were dubbed angels, because of the small likelihood of ever realizing a return. |

STALKING ANGELS

Angel investors are at once difficult and easy to find. The situation is analogous to searching for gold. Generally, it’s difficult to find, but once you hit a vein . . . all of your hard works pays off in a big way. Here are the places to look to find angels.

• Universities. According to Bob Tosterud, executive director of the Council of Entrepreneurship Chairs, a council consisting of business schools with endowed entrepreneurship chairs, even schools with fledgling entrepreneurship programs generally have top-rated professors with ties in business and academia. Angel investors, says Tosterud, tend to hover near these programs because of the high level of new business activity they generate. Tosterud counsels that if you are looking for money, call the nearest university with an entrepreneurship program, and make an appointment to speak with the person running the program. Generally, he says they can point you in the direction of angels.

| A Good Deal: Angel investors often add value in areas where new or emerging businesses need help such as sales, marketing, strategic planning and finance. In addition, angel investors often prove to be an invaluable reservoir of contacts. |

• Business Incubators. According to the National Business Incubation Association (NBIA), there are more than 550 business incubators in North America. At first blush, incubators appear to be mere bricks and mortar that offer entrepreneurs reasonable rents, access to shared services, exposure to professional assistance, and an atmosphere of entrepreneurial energy. But, according to NBIA executive director Dinah Adkins, many business incubators offer formal or informal access to angel investors. While many of these relationships exist for the benefit of businesses actually in the incubator, not all do, and an incubator’s director may offer to make some introductions for you. On the other hand, maybe putting your business in a business incubator is not such a bad idea . . . .

To find a business incubator near you, see the chapter in this book titled Business Incubators. (Add link)

| ACTION STEPS TO FINDING ANGEL INVESTORS Here are 10 actions steps you can take to find angel investors in your area. 1. Call your Chamber of Commerce and ask if it hosts a venture capital group. Many such groups have a chamber affiliation. 2. Call a Small Business Development Center (SBDC) near you and ask the executive director if he or she knows of any angel investor groups. . Ask the SBA if you don’t know where an SBDC is. 3. Ask your accountant. If your accountant doesn’t know, call a “Big Six” accounting firm and ask for the partner handling entrepreneurial services. Ask him or her to point you in the right direction. 4. Ask your attorney. They always know who has money. 5. Call a professional venture capitalist and ask him or her if they are aware of an angels investor group. 6. Contact a regional or state economic development agency and ask if they are aware of an angel investor group. 7. Call the editor of a local business publication and ask if they know of any groups. They often write about such activity. 8. Look at the “Principal Shareholder’s” section of initial public offering (IPO) prospectuses for companies in your area. This will tell you who has cashed out big. 9. Call the executive director of a trade association that you belong to. Ask if there are any investors which specialize in your industry. 10. Ask your banker. If you bank at a small bank, ask the president of the institution. If yours is a larger commercial bank, ask your lender. If you do not have a lender, ask for a lender who works with loans of $1 million or less. A good small business banker will know of such a group because companies that have received an equity investment are good candidates for a loan. A good small business banker will know of such a group because companies that have received an equity investment are good candidates for a loan. |

• Venture Capital Clubs. The tremendous wealth created through the commercialization of technology, and a robust stock market for the past 15 years has resulted in a large number of angel investors who have begun to formalize their activities into groups or clubs. The clubs actively look for deals to invest in and want to hear from entrepreneurs looking for capital.

• Angel Confederacies. Many angels band together in informal groups that share information and deals. Many times members of the group will invest independently, or join together to fund a company. So-called confederacies are not easy to find, but once you find one member, you can gain access to them all, a figure that might top 50 investors.

One word of caution is in order. Formal venture capital groups come in two stripes: those which cater to individual investors or angels, and those which cater to professional, institutional venture capital funds. If you are pursuing angel investors it’s important to pursue the kinds of clubs that will cater to your needs. For instance, the New York Venture Capital Group, in Manhattan, is a vibrant organization. But it caters mostly to professional venture capitalists. By contrast, the Western New York Venture Association in Amherst encourages memberships for individual investors.

| Taking Action: Find at least one angel-oriented networking event in your area and attend. Try to collect at least 10 business cards. And try to give out at least 10 as well. |

FEDERAL SECURITIES LAWS WHICH MAY INFLUENCE YOUR TRANSACTION WITH ANGELS

In 1982, Congress quite accurately recognized that many of the federal securities laws on the books represented an impediment to capital formation for smaller businesses. The result was the creation of Regulation D, which among other things, offered small companies exemptions from federal securities laws for certain kinds of transactions. There are several wrinkles to “Reg D” as it is known, but three important rules which could influence any kind of deal you strike with an angel investor are as follows.

• Rule 504. This rule is the least restrictive of all the federal securities laws exemptions and allows issuers, i.e. companies to sell up to $1 million of securities during a 12 month period, with no restrictions on the number or qualification of investors. In addition, there are no information requirements, and general solicitation and advertising of the offering are permitted. In short, using Rule 504, a company can sell securities to anyone, without providing any information, and still not provoke federal securities laws.

• Rule 505. This rule allows companies to raise up to $5 million, from 35 “nonaccredited” investors and an unlimited number of accredited investors. Accredited investors are also defined by Reg D. There are 16 separate definitions, which range from banks, to employee benefit plans, to wealthy individuals. In the context of this discussion, accredited investors refer to individuals or angels. Individuals are considered accredited if they have a joint or net worth in excess of $1 million, or joint income in excess of $300,000.

Rule 505 imposes some information disclosure requirements on the issuer, unless the securities are sold exclusively to accredited investors.

• Rule 506. Deals structured under Rule 506 are sometimes called unlimited private placements because Rule 506 can be used to raise any amount of capital. An unlimited private placement can be sold to as many as 35 nonaccredited investors and an unlimited number of accredited investors. Rule 506 does impose some so-called sophistication requirements on the nonaccredited investors. Specifically, the company must believe that the nonaccredited investors have the experience or counsel to evaluate the merits and risk of the offering.

Using rules 504, 505, and 506, companies can escape the burden of federal securities laws. However, all states have securities laws as well. What is exempt at the federal level may not be exempt at the state level. If your offering is not exempt at the state level, you may find you have to file the kind of registration statement with state securities authorities which you were trying to avoid at the federal level.

| Don’t Forget: Every state has securities laws too. Selling securities to investors in your state or in another state may provoke two sets of securities laws. Find out if you invoked any state securities laws before you take an investor’s check. |

As with all securities matters, it’s always best to check with a securities attorney before soliciting an offering or accepting money from investors.

TYPES OF ANGELS

The importance of the chemistry between entrepreneur and investor cannot be underestimated. “Ultimately,” says angel investor Rich Bendis, who is also president of the Kansas Technology Enterprise Corporation, “while economics play a big role in a deal, so too does personal chemistry.” In fact, consider that while a banker may completely trust and like an entrepreneur, he or she will not change their lending criteria a single iota because of these feelings. But with angel investors, the situation is completely opposite: if they develop a bond with an entrepreneur, angels can be convinced to do almost any deal.

Because of this phenomena, Bendis says that entrepreneurs must understand the basic investor personality types because it will help them forge the bond which is so vital to closing the deal. While private investors come in many different shades, they can be broken down into five basic types. These are 1) Corporate angels; 2) Entrepreneurial angels; 3) Enthusiast angels; 4) Micro-management angels; 4) Professional angels.

• Corporate Types. Corporate angels are senior managers at Fortune 1000 corporations who have been outplaced or taken early retirement. Stock options and a robust stock market have created an entire new generation of wealthy, or at least wealthier, corporate executives. Corporate angels act like they are looking may say they are looking for investment opportunities, but in reality, they are looking for another job. This doesn’t mean they won’t invest. Bendis says these investors typically have about $1 million in cash and may invest as much as $200,000 into a deal, but some kind of position, usually unpaid at first, comes with the bargain.

Bendis says corporate angels typically make just one investment, unless their last one didn’t work out. And with respect to the one investment they make, corporate angels tend to invest everything at once and tend to get nervous when the hat gets passed their way again.

| Don’t Forget: Angels invest in companies for reasons that often go beyond just dollars and sense. As a result, your appeal must be financial, but also emotional. “We need more than just dollars, sir. We need you to bring your incredible wealth of experience to the table as well. In the long run, it may be even more important than capital.” |

• Entrepreneurial Angels. These are the most prevalent investors, according to Bendis. Most of them own and operate highly successful businesses. Because these investors have another source of income, and perhaps significant wealth from an IPO or partial buyout, they will take bigger risks and invest more capital. Whereas the corporate angel is looking for a job, the entrepreneurial angel is looking for 1) synergy with their current business, 2) a way to diversify their portfolio or in rarer instances, 3) a way to prepare for life after their current business no longer requires their attention. As a result of this orientation, these investors seldom look at businesses outside of their area of expertise, and will participate in no more than a handful of investments at any one time.

According to Bendis, entrepreneurial angels almost always take a seat on the board of directors but hardly ever take on any kind of management duties. They will make fair-sized investments, $200,000 to $500,000, and invest more as the company progresses. However, because of their agenda, when the synergy or the potential they initially perceived disappears, oftentimes so do they.

• Enthusiasts. While entrepreneurial angels tend to be somewhat calculating, enthusiast angels as they are termed, simply like to be involved in deals. Bendis says that most enthusiast angles are 65 or older, independently wealthy from success in a business they started, and have abbreviated work schedules. For them, investing is a hobby, and as a result, they typically play no role in management and rarely ever seek board representation. But because they spread themselves across so many companies the size of their investments tends to be small — from as little as $10,000 to perhaps a couple of hundred thousand dollars. “On the plus side however,” notes Bendis “enthusiasts tend to have a difficult time saying no, and often will bring their friends into a deal.”

• Micro-management Angels. “Micro-managers are very serious investors,” according to Bendis. “Some of them are born wealthy, but by far the vast majority attained wealth through their own efforts.” Unfortunately, this heritage makes them dangerous. Since they have successfully built a company, micro-managers attempt to impose the same tactics they used with their own companies. Though they do not seek an active management role, micro-managers usually demand a board seat. If the business is not going well, they will try to bring in new managers.

Bendis says it’s possible to exploit the behavior patterns of micro-managers, but at a cost. “Specifically, they enjoy having as much control as possible,” he says. “Many will gladly pay for it by putting more capital in the business.”

• Professionals. The term professional in this context refers to the investor’s occupation such as doctor, lawyer, and in some very rare instances, accountant. Bendis says that professional angels like to invest in companies which offer a product or service with which they have some experience: a doctor will look at medical instrumentation companies, a franchise attorney will look at franchise deals, and so on.

These investors tend not to have the need to know what’s going on in the business day-to-day and they do not micro-manage their portfolio companies. In fact professionals rarely ever seek board representation. However, Bendis says, they can be unpleasant to deal with when the going gets rough, and may believe that a company is in trouble before it actually is.

Bendis says professional angels will invest in several companies at one time, and their capital contributions range from $25,000 to $200,000. He adds “They are good for initial investments, but are less likely to make follow-on investments.” Perhaps more than any other category of investor, professionals operate within loosely defined, but clear networks, and they tend to have more comfort investing alongside their peers. Thus, the first professional investor which you find will likely offer a pathway to others. Finally, professionals can also offer additional value when they bring to bear legal, accounting, or financial expertise for which the company would otherwise have to pay hefty fees. Be forewarned, however, because some professionals want to get hired after they invest.

| A Good Deal: Angel investors can often fill the role of de facto financial advisor, and in this role, can lead you to other sources of financings. Once they’re in your court, all you have to do is ask. |

Alternatives to an IPO – Reverse Mergers

| REVERSE MERGERS Definition or Explanation: A privately held company acquires a publicly traded, but likely dormant, company. By doing so the private company becomes public. Appropriate For: Reverse mergers are appropriate for companies which do not need capital quickly, and which will experience enough growth to reach a size and scale where they can succeed as a public entity. Minimum sales and earnings to reach this plateau would be $20 million and $2 million, respectively. Supply: There are thousands and thousands of dormant public companies, sometimes called shells which might be viable merger candidates. By becoming public, a company becomes a more attractive investment opportunity to a wider range of investors. The supply of equity capital is more abundant for public companies than for private ones. Best Use: Reverse mergers can be used to finance anything from product development to working capital needs. However, they work best for companies which do not need capital quickly. Not that reverse mergers take long to consummate. But consummating the initial transaction is usually just the halfway point. Once public, a company generally still has to find capital. Also, this financing technique works better for companies which will experience substantial enough growth to develop into a “real” public company. Cost: Expensive. Compared to a conventional initial public offering, fees and expenses are not that high for a reverse merger. Deals can be completed for between $50,000 and $100,000 which might be 25% of the out of pocket costs that come with a full-blown IPO. In the process of doing the deal however, the acquiring company might give up 10% to 20% of its equity. This is very expensive. After all, it means a company is surrendering ownership just for the privilege of being public. More equity will likely disappear when the company actually raises money. Ease of Acquisition: Difficult, but not as difficult as a conventional initial public offering. Perhaps the most challenging aspect of a reverse merger is trying to create a real trading market for the company’s shares once the deal is done. Range of Funds Typically Available: $500,000 and up. |

THE REALITY OF THE SITUATION

Though initial public offerings are perhaps the most sought-after form of financing, the fact is surprisingly few companies can ever hope to successfully negotiate their way through the tortuous process.

This truth leads to a nasty little Catch-22. Many promising small companies cannot get funding because they are private. However, without funding, they can’t ever hope to grow to the size and scale where they could go public.

| Shop Talk: Investors frequently talk about “exit strategies.” This is a fancy reference to cashing out. Specifically, once an investor puts money into a company, they want to know how they can get their money back out at a profit. |

Why is being a private company anathema to the capital formation process? Because many investors believe that even if the company does well, without an exit strategy for the investors to get their money out of the company, they will never realize a substantial return on their investment. There might be some merit to this thinking. However, the other side of the coin is that the company which is patiently funded so that it is able to realize its true potential will have numerous options for rewarding its shareholders.

A CASE IN POINT

Perhaps the highest and best use of a reverse merger was made by LVA Group.

The company’s founder Dr. Jerry Stephens already had a profitable hospital management business. But he saw an opportunity in free-standing centers offering laser refractive eye surgery to correct myopia, also known as nearsightedness. However, the process was not yet approved and was awaiting the nod from the FDA. “The U.S. was a multi-billion dollar market,” according to Stephens.

To get ready, the company laid plans for financing the roll-out of centers in the United States and bought part of a laser surgery center in Toronto, where the process was already legal.

Considering financing alternatives, Stephens believed he could cobble together an IPO, but concluded that it was highly unlikely for a new and untested concept. What if the FDA approval was delayed?

But with a reverse merger, Stephens only had to convince the controlling shareholder of a public shell that the reward was worth the risk. And the controlling shareholder of the shell company which Stephens was talking with happened to agree.

In the resulting deal, Stephens bought stock in the shell company in exchange for LVA Group’s assets. At the end of the day, Stephens had a majority position in the shell company, and the shell company had the operating assets of his company. The public company then changed its name to LVA-Vision to reflect the deal and the future course of the business.

| Don’t Forget: A reverse merger is not an end in and of itself. It is a technique or tool, which makes a company more financeable. |

Two months after the deal, the FDA approved the laser refractive procedure used by LVA, and Stephens was off and running. Almost immediately, Stephens raised nearly $500,000 privately. He also used his publicly traded common stock to buy the remaining interest in the Toronto facility. The private capital he raised, combined with favorable lease terms on surgical laser equipment helped Stephens roll out seven new surgery centers in the South and Midwest. After a brief honeymoon on Nasdaq’s Bulletin Board, LVA Vision moved up to Nasdaq’s SmallCap.

In a climaxing deal, LVA used its stock to purchase a chain of refractive surgery centers from another company. To acquire the company, LVA issued several million of its own shares and in return got the other company’s 19 wholly owned and operated refractive surgery centers around the country. As a final bonus, the company that LVA bought had $10 million in the bank when the deal was inked.

Today, LVA Vision is the largest provider of vision treatment procedures in the United States.

THE BENEFITS OF GOING IN REVERSE

Here are some of the primary benefits entrepreneurs and their companies can reap with a reverse merger transaction.

• Reverse mergers are impervious to market conditions. Conventional IPOs are risky for companies to undertake because the deal depends on market conditions over which senior management has absolutely no control. That is, if the market is off, the underwriter may pull the offering. The market doesn’t even need to plunge wholesale. If a company in registration participates in an industry that’s making unfavorable headlines, investors may shy away from the deal, causing it to run out of gas on the runway.

But with a reverse merger, the deal rests on whether or not the people that control the shell like the private company and desire to be acquired by it. Market conditions have almost no bearing on the situation.

| A Good Deal: Even if the market crashes while you are working on your reverse merger, it probably won’t kill your deal. For the shell company, with few assets and little or no story to tell, a good merger is good news and worth pursuing, no matter what market conditions are. |

• Compressed timetable. Regular initial public offerings can drag on for a year or more, between when the idea pops into the chief executive’s head until he or she actually gets a check. Unfortunately, when a company is making the transition from an entrepreneurial venture to a real public company fit for outside ownership, senior management’s time is at its most valuable. Time spent in seemingly endless meetings and drafting sessions can have disastrous effects, and even nullify the growth upon which the offering is predicated. In addition, during the many months it takes to put together an IPO, market conditions can deteriorate, closing the “IPO window” on a company.

By contrast, conditions permitting — which means among other things, two extremely interested and willing parties — a reverse merger can be completed in 45 days.

• Reduced expenses. For a real IPO, it can cost as much as $200,000 just to get a preliminary prospectus on the street. To actually get the deal to the closing table, the costs increase. A reverse merger, however, can be done for $50,000 to $100,000.

• Corporate income tax shelter. Many shell companies have what is known as a tax loss carryforward. What this means is that a loss incurred in prior years can be applied to income in future years. When this occurs, the future income is sheltered from income taxes. Since most active public companies become dormant public companies through a string of losses, or at least one large one, there’s a better than average chance the shell you meet will offer this opportunity.

(As discussed in the next section, however, the shell company’s previous history can rub off on you, which turns out to be one of the biggest drawbacks of reverse mergers.)

| Don’t Forget: In addition to fees, a reverse mergers will also cost you precious points of equity in your company. The shareholders of the public company get a stake, and the deal makers who control the shell get a stake as well. |

• More Ways to Raise Money. The primary reason to do a reverse merger to begin with is the greater number of financing options which become available to companies once they are public. Some of these include:

- The issuance of additional shares in a secondary offering.

- Exercise of warrants. Warrants are options, which give the holder the right to purchase additional shares in a company at predetermined prices. When many shareholders with warrants, which a public company can easily issue, exercise their option to purchase additional shares, the company receives an infusion of capital as shown above.

- Private Offerings. Many, many more investors will step up to the plate for a private offering of shares, once they know there is some sort of mechanism in place for them to resell their shares if the company succeeds. Most investors realize that even a successful company may not be able to go public if market conditions are off. But a company that is already public . . . that’s a different story. If it succeeds, the likelihood of developing a market for its common stock that accurately values the company and allows the investor to sell their shares is much much better.

THE DRAWBACKS OF A REVERSE MERGER

Reverse mergers aren’t for everyone, however. There are several drawbacks to this financing technique. Among the disadvantages:

• Image. Reverse mergers have accumulated their share of controversy over the years. There are several reasons for this. First, most reverse mergers start with dormant public companies. Most of the time, they fell into dormancy because of failure in their line of business. As a result, there may be an angry group of shareholders somewhere in the deal. Second, the chances of some irregularity occurring in the trading, most likely unknown to the company, are high with reverse mergers. The reason is most reverse transactions initially trade on the Pink Sheets or the Bulletin Board, the least regulated tiers of the market.

• Unknown shareholders. At the end of the day, the private company which acquires a public one is left with a shareholder base it does not know and has no previous interaction with. These shareholders can place significant downward pressure on a company’s stock by continually selling their shares as a new trading market develops. Also, creditors, or other parties which suffered from the failure of the predecessor company, can start to come out of the woodwork, and make claims against the new management.

• Indirect route to capital. Reverse mergers represent a way to make a company financeable not necessarily finance it per se. Though they are theoretically quick and easy, like any securities transaction, reverse mergers contain enough wrinkles to make the process drawn out and lengthy. But in most instances, just consummating the reverse merger transaction is only the halfway point in a company’s pilgrimage to growth capital. When it’s done, the company still has to go out and beat the bushes for the cash they need.

| Shop Talk: The controlling shareholders of a shell corporation will most likely insist on owning a small stake in the deal going forward. This “trailing interest” is simply a cost of doing business. |

• Difficult to become a real public company. Despite the fact that an exciting private company has taken over control of a dormant public company doesn’t mean other investors will sit up and take notice. In fact, the only investors who tend to care about the change in control are the ones who invested in the original company. Oftentimes, their interest is mercenary: they simply want to know when the new company will succeed to the point where they can get their money back.

As a result of this relative obscurity, most reverse mergers find their stock doesn’t trade much. Moreover, company executives and principals find they have a hard time attracting investors to their stock to create the kind of trading and liquidity which is the benchmark of a real public company.

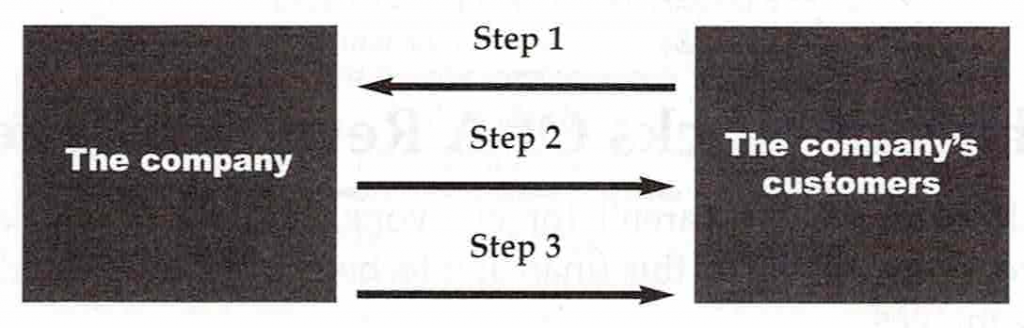

| THEORY INTO PRACTICE: THE MECHANICS OF A REVERSE MERGER In the diagram below, the hypothetical public company has 1 million common shares outstanding prior to any sort of transaction with a private company. Of these 1 million shares, 500,000 are owned by public investors, and 500,000 are owned by the person or persons who control the public company. Once a deal is struck for the private company to acquire the public one, here’s how it might be consummated in a three-step process: 1. The public company issues 9 million shares of common stock to the person or persons who own the private company. Now, what is the ownership structure of the public company? There are now 10 million shares outstanding. Of these, 9 million or 90% of the company is held by the owner of the private company. Another 500,000 shares, or 5% ownership of the company, are held by the person or person who controlled the public company. And the public investors, hold the other 500,000 shares or 5% of the company. Note that prior to the merger, the public-owned 50% of the public company, but after the merger, they owned just 5%. 2. The 9 million shares of common stock are usually issued to the shareholders of the private company in exchange for something. In most reverse merger transactions, the private company: a) contributes all of its assets to the public company; b) issues shares of its own to the public company, or c) buys the shares outright from the public company at a nominal price. 3. The public company then changes its name, usually to the name used by the private company, to reflect the change in its business. |

STRATEGIES & NEXT STEPS FOR A REVERSE MERGER

If a reverse merger still sounds like a good idea to you, here are the steps you need to take.

• Find a shell company. You can find a shell company through the usual suspects. As a first stop, ask an attorney. Every metropolitan area has a law firm with a securities practice. Many times these firms have a dormant public company literally sitting on one of the partner’s bookshelves.

Another alternative is an accountant. People who control shell companies tend to keep the financial statements, such as they are, up to date. This brings accountants into the loop. Like the attorneys, they know where the bodies are too.

Another source is financing consultants. In fact, many financing consultants actually have a couple of shell corporations, and upon request, can manufacture a clean public shell. Made-to-order shells, without the baggage of a business failure in its background, can sometimes be the way to go.

But, there’s often a cost involved. That is, you will most likely end up with the financing consultants as minority shareholders in the new company holding somewhere between 2 and 5 percent. However, in almost any reverse merger transaction, the principals of the shell company keep a small equity position in the company going forward. Therefore this surrender of equity is simply a cost of doing business.

• Devise your financing strategy. As mentioned several times already in this chapter, a reverse merger is an indirect route to raising capital. Entrepreneurs must consider first how additional capital will be raised after the deal is done.

As mentioned above, a public company can issue and exercise warrants. Some public shell companies already have warrants issued and outstanding which have the underlying common stock shares registered with the Securities and Exchange Commission. This is much easier, and much more valuable to a company that wants to raise capital with warrants. If the newly public company has to create and issue warrants, the road to getting them exercised will be trickier, but still possible. In short, to exercise warrants where the underlying common shares are not registered, the exercise will require the assistance of a brokerage firm, and will have to occur in a state where there is no registration requirement for issuance of shares of $1 million.

| Don’t Forget: If you need all the bells and whistles of a true public company, you can spend as much time and money on the back end of reverse merger as you would on the front end of a conventional initial public offering. |

If you are going the private offering, i.e., an offering sold to select individuals rather than through a sale directly to the public at large, then the deal must be carefully structured. Specifically, the amount of stock owned by investors that the new owners do not know, and cannot influence — must be diminished so that a stable quote can be established. Usually, this is done by reducing the percentage of the total number of shares which these investors own (See Sidebar Above, The Mechanics of a Reverse Merger) By doing so, the private investors can be offered stock at a discount to the market price as an added incentive.

For example, if the stock is $7.00, the private offering offers investors common stock at $5.00. This incentive evaporates when sell orders flood the market, and the market price of the stock drops to $5.00.

Of course, a smart investor knows they can’t simply load up on $5.00 stock in a private placement and turn around and sell it out on the public market at $7.00. There simply aren’t that many buyers to support that kind of selling. But the point is, it’s much easier to sell common stock to investors at $5.00 in a private offering when the market price is $7.00 as opposed to trying to sell common stock privately at $5.00 what the market price is $4.00.

• Clean up your act. Unfortunately, there’s a stigma attached to reverse mergers. LVA-Vision’s Stephens, who used the technique to brilliant effect, said that although it worked for his company, “there’s definitely, another side to these deals. If it wasn’t for my longstanding reputation in the medical community, our deal might have been perceived differently.” Largely, the bad rap stems from the fact that reverse mergers are not understood says Stephens.

Accordingly, entrepreneurs contemplating such a transaction, can and should take steps to elevate the profile of their “new” company. Specifically:

1. Hire a national accounting firm. One of the reasons the “big five” fees are high, is because they inspire a lot of comfort among investors, traders, and regulators. If you saved a lot on fees at the front end, this might be worth investing in on the back end.

2. Hire a prestigious law firm. It’s almost a certainty that the attorney who helps you with your reverse merger transaction, if he or she is an expert in the process, will not be with a prestigious downtown law firm. And though you may be reluctant to switch from a competent and trusted counselor after the deal is over, for the sake of the company and its credibility, it might be a good idea. When deciding whether or not to get involved in your offering, many investors and brokers will judge your firm by the company it keeps. An unknown law firm makes a neutral to a negative impression. But a well-known and powerful law firm sends an unmistakable message.

• Start with a clean shell. As mentioned, there are many shells which are created for the express purpose of merging with a private company. These shells have no predecessor entities, and as a result, little baggage in the way of a business failure or other skeletons in the closets.

• Check your greed. The great rallying cry of the 1980s popularized by Hollywood’s oily takeover artist, Gordon Gekko, “Greed is good,” doesn’t quite apply with a reverse merger. It’s possible to structure a reverse merger so that at the end of the day, the public owns 2% of the company, and the remaining 98% is controlled by the owners of the private company which acquired the shell. Unfortunately, there’s almost no incentive for any other investors to get involved if the only people who truly benefit are the insiders. The lesson is, if you are going to get the public involved with the intention of engaging in a truly symbiotic relationship, you’ve simply got to leave some value on the table.

In many ways, the reputation of reverse mergers is similar to the notoriety which junk bonds had during the 1980s. Junk was used by corporate raiders to buy companies and break them up. But junk bonds also nurtured an entire generation of exciting growth companies and made material and profound impact on the economy in terms of wealth and employment.

Remember, reverse mergers are simply a technique. The ultimate goodness or badness of the deal depends on how wisely it is deployed.

| Taking Action: Start calling attorneys and accountants and ask them if they are aware of a clean shell company. You should locate something in less than 10 calls. |

Royalty Financing

| Definition or Explanation: Royalty financing is an advance against future product or service sales. The advance is paid back by diverting a percentage of the product or service sales back to the investor who issued the advance. Appropriate For: Established companies that have a product or service or emerging companies about to launch a product with high gross and net margins. Also companies with elastic pricing, i.e. the ability to raise prices without any impact on sales. In addition, royalty financing is most appropriate for companies which experience a quick cause and effect between marketing activity and sales increases. Supply: Substantial. Royalty financing can appeal to investors who typically do not make investments in private companies. In addition, angel investors, venture capitalists, and even state, city, or regional economic development agencies can be sold on the concept of royalty financing. Best Use: Financing intensive sales and marketing activities. Cost: Inexpensive for companies with high margin products or services. Ease of Acquisition: Relatively easy because the technique appeals to a wide variety of investors. In addition, because royalty financing is essentially a loan, it generally does not provoke state and federal securities laws. Range of Funds Typically Available: $50,000 to $1 million |

ROYALTY FINANCING: THE SECRET WEAPON

Many companies still in their formative stages face a difficult dilemma when looking for equity capital. Equity investors, whether they are angels or venture capitalists, often demand a big piece of the company because of all the risk they are incurring. The dilemma is compounded by the fear that, if the company gives up 30%, 40%, or even 50% of the company on the first round of outside financing, there’ll be nothing but a grubstake left by the time the company goes public.

Enter royalty financing which eliminates the dilemmas of equity financing by removing them from the picture altogether, according to Peter Moore, founder of Banking Dynamics, a consulting firm in Portland, ME, which helps companies raise capital, and a proponent of the royalty financing technique. “Instead of selling equity,” says Moore, “a company simply pledges a piece of its future sales against an advance provide by the investors.”

| A Good Deal: Royalty financing is a good deal for investors who typically do not invest in early stage companies because they are able to taste the fruits of their investment almost immediately, and if the company prospers, every month or quarter thereafter. |

A CASE IN POINT

Here’s how Moore structured financing to help a software company turbocharge its sales.

Rather than angel investors, Moore approached the Greater Portland Building Fund, and Coastal Enterprises, Inc., quasi-public economic development organizations charged with developing business in the state.

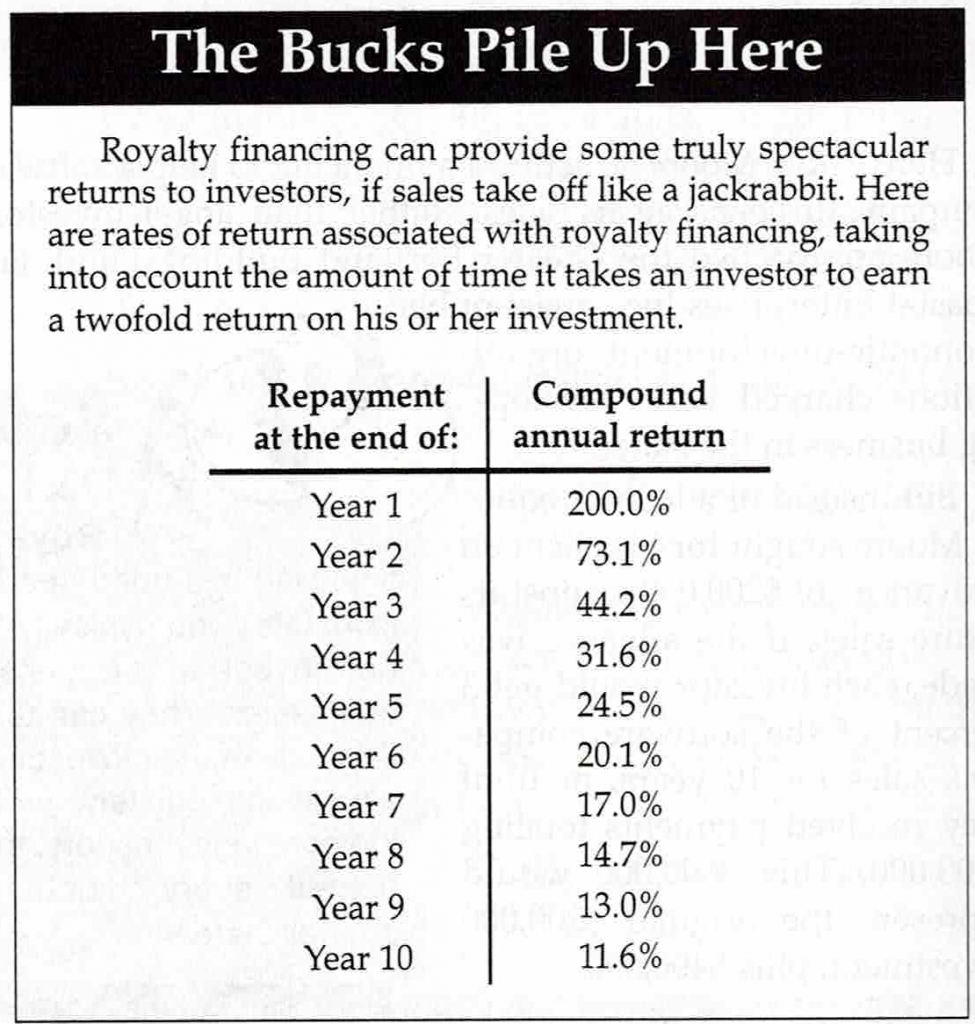

But instead of a loan or equity, Moore sought an “advance” of $200,000 for his client against its future sales. If the advance was made, the investors would each get 3% of the software company’s sales for 10 years, or until they received payments totaling $600,000. This $600,000 would represent the original $200,000 investment, plus $400,000 more.

At the broadest level, in order for the investors to get the agreed-upon $600,000 within the maximum allowable time frame, the software company would have to generate total sales of $20 million over 10 years. Although the software company had less than $1 million in sales at the time, it had over the course of its three-year life, double sales each year. “This was a big selling point,” says Moore. Moreover, he says that investors were comforted by the fact that the company’s software program, which helps companies manage hazardous waste streams, meant there were 300,000 potential customers.

The deal was structured so that the time frame was flexible — up to 10 years to make repayment — but the return — $600,000 — was not. Because of this, the return which the investors could earn was variable as well, and ranged from pretty good to exceptional. Specifically, if the software com pany repaid the advance in 10 years the investors would earn a compound annual return of 11.6% on their investment. If however, the company’s sales mushroomed, and $600,000 was paid to the investors in five years, their compound annual return mushroomed also to 24.5% — a rate which even an institutional venture capitalist would have to admire.

It took Moore and his client about four months to hammer out all the details of the deal. One of the key terms that Moore negotiated for was a delay in the commencement of royalty payments. Specifically, royalties did not start to accrue until 90 days after the deal closed. In addition, the actual royalty payments did not have to be paid until 60 days after [italicize after] the revenues were recognized. “All in all, there were five months from the time the company received the financing, and when the first payment was due. This gave them the time they needed to put the capital to work and start producing sales.”

| Don’t Forget: The initial advance from the investor to the company is a loan, not an equity investment, and as a result, does not in general provoke securities laws. |

IT’S A GOOD THING

Royalty financing is extremely flexible and can be structured in a myriad of ways. But regardless of the final structure, the technique delivers a host of advantages that entrepreneurs should carefully consider before rushing to sell equity in their companies.

• Attractive to Individual Investors. Generally speaking, it’s difficult for most individual investors to get involved in financing private companies. Many times, they don’t have enough capital to make a difference. Many times individual investors don’t have the minimum net worth requirement established by state securities regulators. But perhaps one of the biggest barriers is that buying straight equity general only provides a return if the company gets acquired or goes public, two very big ifs. Moore speculates that a monthly or quarterly return — which happens as long as sales occur — would be more preferable to individual investors than the total absence of a yield and zero liquidity that is typical of early-stage venture deals.

| Shop Talk: The concept of ‘revenue recognition’ takes on greater significance within the context of a royalty financing because it defines the payments to the investor. Should revenue be recognized when the customer agrees to purchase the product or when they pay for it or perhaps after a 30 day return period has elapsed? |

• Bypasses Securities Laws. Because the royalty advance is, at the end of the day a loan, it does not, in plain vanilla form, provoke any state or federal securities laws. Most equity financing, where companies sell shares to individual investors requires complex filings that mean significant legal and accounting fees.

• Increases Future Financing Options. A company funded by royalty payments increases its financeability down the road. If the funds do in fact ramp up sales, the company becomes a more attractive candidate for additional financing. In addition, sometimes the presence of one kind of equity investor precludes the participation of other kinds. For instance, a company financed with institutional venture capital funds cannot, in most cases, ever go back to raising money from individuals. But by “saving” itself for outside investors to a later round of financing, a company keeps its options wide open.

• Preservation of Equity. The royalty structure preserves the equity positions of the founders. Remember, there are only 100 percentage points to go around, and they begin to disappear with alarming ease once a company begins to raise outside capital. In addition, when founders are able to hold on to a significant portion of the ownership they may be more incentivized to make it successful, than entrepreneurs who have given away most of the store.

NOT FOR EVERYONE

It may sound as if royalty financing is a panacea. Unfortunately, it’s not. There are several instances where royalty financing will not work.

• Thin Margins Are A Problem. If a company’s gross margin (sales less cost of goods sold) is just 10%, and 6 percent goes to royalty payments, then the remaining 4 percent doesn’t leave much room for making any money. In the above example, the software company which Moore financed had a gross margin of 90%. With margins this wide, it could comfortably give up 6 percent of the sale.

• Competitive Pricing. Royalty financing works best for companies whose pricing is fairly elastic. If you can raise your prices to cover the cost of the financing, the marketing of the product, and not lose any customers, you are a better candidate than a company where customers are price sensitive.

• Lengthy Sales Cycles. Royalty financing won’t work for companies that do not see a rather immediate cause and effect between marketing efforts and sales. “You’ve got to be able to turn on sales like a spigot,” says consultant Moore. Otherwise, one of the primary benefits for which investors are in the deal — namely a monthly royalty check — becomes seriously compromised. The one thing a growing company doesn’t need are unhappy investors.

This limitation goes even deeper. Royalty financing is not appropriate for financing product development. After all, making something new is tricky. Success may be elusive, or — and how often does this happen? — it takes much longer to develop the product or service than originally anticipated.

• Good Marketing Skills. Obviously, just having a product can’t win the day. For companies to effectively use this technique, they’ve got to be able to sell [italicize sell] and market [italicize market] their wares. “Obviously,” says Moore, “you have to be able to inspire confidence among investors that you have the skills and experience that will move products or services off the shelf frequently and quickly.”

| Taking Action: To get a primer on royalty financing, send a self addressed stamped envelope to Mr. Peter Moore, Banking Dynamics, 97 A Exchange Street, Portland, ME 04101, 207-772-2221. |

Community Development Financial Institutions

| Definition or Explanation: Community Development Financial Institutions (CDFIs) provide primarily loan financing to businesses in areas seeking economic development. CDFIs make loans that are generally “unbankable” by traditional industry standards. Appropriate For: Start-up to established companies that can demonstrate the ability to repay a loan, but whose loan proposal is unbankable because of past credit problems, size of the loan request, limited equity from founders, or limited collateral. Supply: Good. There are hundreds of CDFI’s in urban, rural, and reservation-based communities with billions of dollars to lend. Unfortunately, despite their numbers, CDFI’s can sometimes be difficult to track down. Best Use: To start a new business or to expand an established one. But also, where the application of the proceeds can create a second bottom line in the form of community job creation, the introduction or preservation of a service that is vital to a community, or stabilizing a community in decline. Cost: Relatively inexpensive. Most CDFI loans are priced according to risk, as opposed to the cost of funds. Since CDFI loans tend to be riskier than bank loans they tend to cost more as well. Typical pricing may be from a half to three percentage points higher than conventional loan rates. Ease of Acquisition: Easier than commercial lenders but challenging, since for loans, a company must still undergo the scrutiny of traditional credit analysis. The challenge of securing CDFI financing is sometimes compounded by the relatively narrow focus and agenda which these institutions may maintain. Range of Funds Typically Available: $25,000 to $500,000. |

THE POWER OF THE PEOPLE

The idea behind a Community Development Financial Institution (CDFI) is simple and powerful. In a nutshell, this idea is that a community will make viable loans to businesses that can help it grow and prosper.

That was certainly the case with two unlikely entrepreneurs from the Northwest. Sawmill managers Mike Brine and Dave Miles always had the itch to work for their own company instead of someone else’s. As a result, when the opportunity arose to take control of a closed down mill, and call it their own, the two didn’t waste any time looking into it.

The only problem is when opportunity knocks, it usually wants money. In the case of the two rough-hewn entrepreneurs, the opportunity required a capital commitment of $100,000.

There were plenty of risks. First, the business, despite its previous heritage, would be a pure start-up Second, operating a sawmill was a risky business. Mills had closed by the score throughout the Pacific northwest. By almost any yardstick, the deal which Brine and Miles had in mind was not bankable by any stretch of the imagination. But the Cascadia Revolving Loan Fund, a community development financial institution in Seattle had a different perspective.

| A Good Deal: Although CDFI financing is generally more expensive than conventional loan financing, it is often still a good deal, because the alternative is often no financing at all. |

According to loan officer Josh Drake, Cascadia, true to the credo of a CDFI saw its way through the risks and came through with the $100,000 financing package. The deal consisted of a $25,000 five-year term loan, and a $75,000 equity investment. Drake says that the equity investment, though unusual for a community loan development fund by historical standards, is a growing trend, and a positive one, since equity investments do not carry the regular interest payments which can be so crippling to a new enterprise.